Survival Strategies: How Women Made Every Dollar Count During the 2008 Crisis

Article Note

This article examines how women used 2008 crisis survival strategies inside the home, turning budgeting, caregiving, meal planning, bill prioritization, emotional labor, and unpaid household work into ways of making every dollar count during a period of economic instability.

How Women Made Every Dollar Count During the 2008 Crisis

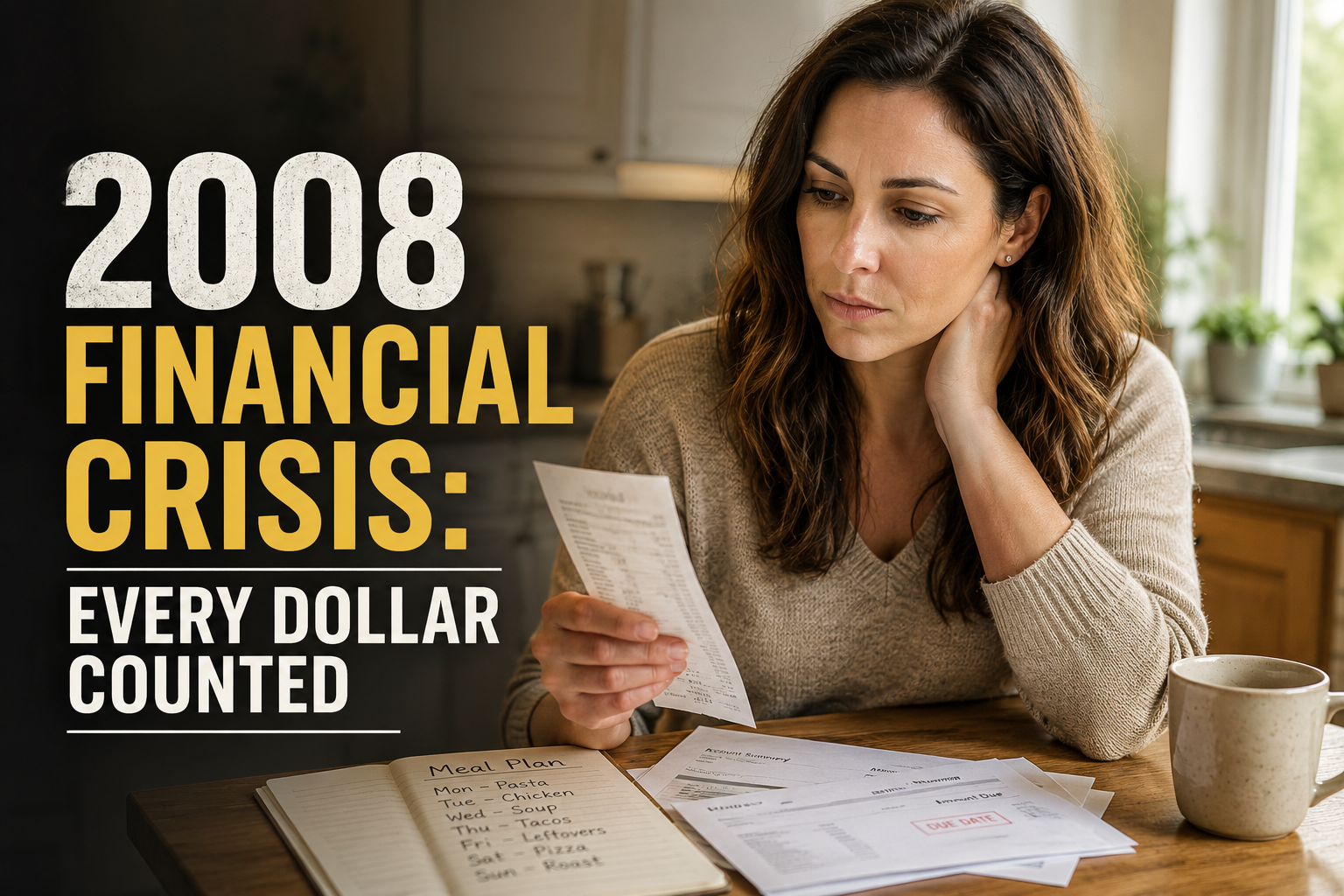

During the 2008 financial crisis, survival did not happen only in banks, workplaces, or housing markets. It also happened at kitchen tables, in grocery aisles, inside overdue bills, and in the quiet calculations women made to keep family life from falling apart.

For many women, making every dollar count became more than a budgeting habit. It became one of the most important 2008 crisis survival strategies inside the home, shaped by scarcity, care, restraint, emotional pressure, and the responsibility of keeping the household functioning when income, wealth, credit, and confidence were under stress.

The crisis is often remembered through collapsing financial institutions, troubled mortgages, unemployment, falling home values, and the loss of family wealth. Those forces were real and decisive. But they do not tell the whole story of how families actually endured the recession day by day.

Inside homes, the crisis took another form.

It appeared in shorter grocery lists, delayed bills, simplified dinners, canceled outings, careful credit card use, postponed personal needs, and the effort to protect children from the full emotional weight of financial instability.

This article begins from that less visible layer of the crisis: the domestic engineering of survival. It examines the unpaid, repeated, and emotionally demanding work women often performed when every grocery choice, every bill decision, every meal adjustment, and every protected family routine became part of the household response to economic collapse.

The goal is not to turn hardship into a list of money-saving tips. It is also not to romanticize women’s ability to endure sacrifice. The point is to recognize that, during the 2008 crisis, many women performed real economic labor that was rarely named as such: managing scarcity inside everyday life.

Making every dollar count meant deciding, again and again, what needed to be protected first. Food, housing, transportation, utilities, children’s needs, health, debt, small signs of normalcy, and basic dignity all competed for space inside compressed budgets.

This kind of management required calculation, but also care. It required creativity, but also renunciation. It required discipline, but also emotional strength. The woman who compared prices, reorganized meals, delayed purchases, reduced waste, protected children from fear, and kept the household moving was not merely “saving money.” She was helping transform economic instability into possible family continuity.

The central question of this article is simple: how did the 2008 crisis force women to turn the everyday budget into a territory of active survival?

The answer rests on one essential idea: many families got through the crisis not only through major financial decisions, but through repeated, silent, and emotionally costly microdecisions made inside the home.

That is the hidden story of 2008. Many families did not survive only because they spent less. They survived because women often engineered survival from within the household, turning ordinary routines into a system of protection when the larger economy no longer felt reliable.

Quick Answer

During the 2008 crisis, many women helped families survive by turning budgeting, shopping, caregiving, meal planning, debt avoidance, and daily restraint into household survival strategies. Making every dollar count was not just frugality. It was unpaid economic labor that helped protect food, shelter, routine, dignity, and emotional stability when income, wealth, and confidence were under pressure.

Key Insights

The 2008 crisis showed that household survival was not built only through major financial decisions. It was also built through repeated microdecisions that many women managed inside the home, often without recognition as real economic labor.

- Making every dollar count became a household defense mechanism, not just a budgeting habit.

- Women often managed scarcity through groceries, meals, bills, children’s routines, emotional labor, unpaid care, and constant financial vigilance.

- Spending less frequently required more work: more planning, more cooking, more comparison, more substitution, more negotiation, and more mental load.

- The household became a frontline of the recession, where economic pressure entered grocery lists, overdue bills, simplified meals, canceled plans, and daily routines.

- These 2008 crisis survival strategies helped many families protect food, housing, dignity, and basic stability, but they also carried emotional costs.

- The recovery story of 2008 is incomplete if it ignores the unpaid, invisible survival work women performed to keep families functioning.

- For many women, the experience of scarcity shaped later attitudes toward debt, saving, emergency funds, risk, safety, and financial independence.

Chapter 1 — When the 2008 financial crisis turned everyday life into permanent calculation

Why everyday life becomes financially intense when crisis enters the household

In times of crisis, making money last is also a form of leadership. During 2008, many women transformed budgeting, consumption, and routine into survival strategies, sustaining entire families through small and exhausting decisions. To understand the weight of this, it is necessary to look at household management not as a detail, but as economic intelligence applied in a scenario of scarcity.

When an economic crisis enters the home, it rarely arrives as an abstract concept. It arrives as a postponed purchase, a bill that has to wait, a grocery trip made with more attention, a difficult conversation about what still fits into the month. The mechanism is simple, but profound: when income becomes uncertain and prices, debts, or obligations continue to exist, everyday life stops being routine and becomes permanent calculation.

The 2007–2009 recession created exactly this environment. The Bureau of Labor Statistics recorded that the U.S. unemployment rate rose from 5.0% in December 2007 to 9.5% in June 2009, reaching 10.0% in October 2009, after the official end of the recession. This figure does not describe only the labor market. It helps explain why so many families began living with fear of income loss, reduced hours, layoffs, more difficult credit, and falling economic confidence.

Inside the home, this kind of pressure changes the function of the budget. Before, the budget may serve to plan, compare choices, and organize goals. In a crisis, it begins to function as triage. The question stops being only “what do we want to do with the money?” and becomes “what needs to survive first?” Food, housing, transportation, childcare, medication, debts, basic bills, and small family commitments begin competing for space within an increasingly smaller margin.

This change is especially important for understanding the role of women. In many families, they already occupied the center of household management before the crisis: they tracked shopping, organized meals, managed children’s needs, noticed when something was missing, and adjusted the routine so the household could keep functioning. When the recession tightened, this everyday position became an emergency function. What might once have seemed like ordinary management began to carry expanded economic weight.

The crisis did not ask only for major cuts. It demanded constant attention to small leaks. A cheaper brand. A repurposed meal. An avoided route. One fewer trip to the grocery store. A reorganized payment. A small luxury cut to protect an essential bill. Seen in isolation, these choices seem minimal. Repeated every day, they become a silent infrastructure of survival.

The Federal Reserve, in analyzing family finances between 2007 and 2010, recorded a 7.7% decline in real median family income before taxes. The same survey showed an even deeper loss in median family wealth during the period, reflecting the combined impact of the recession, falling assets, and the housing crisis. For everyday life, this meant many families were not only earning less; they also felt less protected by wealth, their home, savings, or the expectation of a quick recovery.

This is where everyday life becomes financially intense. The intensity does not come only from the lack of money, but from the impossibility of deciding without consequence. A simple purchase gains a shadow. A small expense begins to be compared with another. A dinner out can turn into guilt. A toy, a uniform, a repair, or an appointment can require renunciation in another area. The home becomes a small economy on alert.

This dynamic also helps distinguish this article from a generic reading on frugality. The theme here is not the virtue of saving. It is the pressure of managing lack when the broader economy fails. In dialogue with Article #56 — “Why Financial Crises Always Come Back — Historical Patterns and Lessons for Women”, this chapter moves the crisis from the historical pattern to the place where it becomes intimate: the household routine. The historical pattern explains the repetition of crises; this analysis shows how that repetition crosses the kitchen table, the shopping cart, and the mind of the person who needs to keep the home standing.

The cognitive closure of this first movement is essential: when the crisis enters the home, ordinary life stops being neutral. Every everyday decision begins to carry a larger question about protection, risk, and continuity. The woman who calculates, compares, delays, and reorganizes is not merely “being careful.” She is translating a macroeconomic crisis into domestic decisions of survival.

How small spending decisions begin to carry outsized emotional and practical weight

The second layer of the problem appears when small decisions begin to carry disproportionate weight. In stable periods, choosing a brand at the grocery store, reducing an occasional expense, or postponing a purchase may seem like mere preference. In periods of crisis, the same choice gains another density. It begins to represent protection, fear, priority, and often guilt.

The mechanism is the compression of the financial margin. When the family has room for error, small decisions do not threaten the structure of the month. But when the margin disappears, every expense begins to compete with harder needs. Money stops being only a means of purchase and becomes an instrument of containment. It needs to cover the present, anticipate risks, and preserve some security for what may still get worse.

The Pew Research Center, in 2010, observed that the Great Recession led many Americans to revise expectations about retirement, their children’s future, home values, consumption habits, and family financial recovery. The report also pointed to a “new frugality” in spending and debt patterns. This observation helps contextualize the emotional environment of the time: it was not merely about families cutting expenses out of prudence, but about a broad shift in the way people imagined security, the future, and consumption.

For many women, this shift materialized in decisions that seemed too small to enter the official narratives of the crisis. Buying less meat. Replacing fresh products with cheaper options. Using coupons. Avoiding stores where the temptation to spend would be greater. Postponing clothes, gifts, home maintenance, or personal care. Reducing travel. Turning leftovers into planned meals. Holding back one’s own desire to preserve the children’s routine.

These choices had practical weight because they protected the household’s minimum functioning. But they also had emotional weight because they required repeated renunciation. The woman was not managing only numbers. She was managing the meaning of every cut. What can be removed without hurting too much? What needs to be maintained so the children do not feel it as much? What can wait without becoming a bigger problem? What is a real need, and what is an attempt to preserve dignity?

This boundary is delicate. In times of scarcity, “necessity” stops being a fixed category. A small purchase may be financially dispensable, but emotionally important. A simple birthday, a favorite food, a piece of clothing for an interview, a school activity, or a modest gift may seem like small expenses on paper, but function as symbolic protection against the feeling of decline. Women’s management of scarcity often involved deciding which small signs of normalcy still deserved to be preserved.

That is why “making every dollar count” cannot be read as a light phrase. During the 2008 crisis, making every dollar count meant assigning a function to every expense. The dollar used at the grocery store was not just a dollar. It was an attempt to feed with less. The dollar saved on transportation was an attempt to protect another bill. The dollar not spent on personal care could become silence, fatigue, or a feeling of disappearance. The dollar directed toward children could carry the desire to prevent the crisis from fully invading childhood.

Official data helps explain why this weight grew. The BLS reported that, in the fourth quarter of 2008, the unemployment rate reached 6.9% and the number of unemployed people reached 10.6 million, a sharp increase from the previous year. This advance in job insecurity created an environment in which even families still employed could act as if loss were near. Economic fear began to shape decisions even before income actually fell.

This anticipation of risk is an important part of household behavior during crises. The family does not necessarily wait for the worst to happen before beginning to cut. Often, it begins to pull back because it perceives signs: a nearby layoff, fewer overtime hours, neighbors losing homes, colleagues without work, news about banks, a housing market in crisis, more restricted credit. The woman who already manages everyday life begins to operate with a permanent question: “What if next month is worse?”

This question changes the tone of life. The grocery store stops being only a place to shop and becomes a space of forecasting. The electricity bill stops being only an obligation and becomes an indicator of control. The credit card stops being a convenience and becomes a risk. The small spontaneous expense stops being pleasure and becomes a possible threat. Everyday life narrows because the crisis turns every decision into a signal.

Here, institutional evidence and household experience meet. Falling income, unemployment, and loss of wealth do not affect only national spreadsheets. They reorganize financial sensitivity inside the home. The real reader recognizes this pattern when she remembers periods in which every purchase had to be justified, every outing had to be calculated, and every small mistake seemed capable of disorganizing everything.

The closing point of this section is that small decisions become large not because of their isolated value, but because of the pressure around them. In a crisis, the weight of an expense is not only in its price. It is in what it prevents, the fear it activates, the bill it competes with, and the responsibility of keeping life functioning despite a minimal margin.

Why surviving a downturn starts with reorganizing ordinary routines, not just large expenses

The third layer of the chapter shows why survival does not begin only with major cuts. In a recession, it is natural to imagine that the center of adaptation lies in the largest expenses: home, car, debts, insurance, tuition, major purchases. These items matter a great deal. But everyday financial life is also sustained by smaller, repeated, and cumulative routines. When the crisis tightens, reorganizing those routines becomes one of the first forms of defense.

The mechanism is the accumulation of micro-adjustments. A family may not be able to immediately change the mortgage, rent, or main debt. But it can change what it buys, when it buys, how it cooks, where it goes, how often it uses the car, which commitments it keeps, which requests it refuses, and which small comforts it suspends. This field of daily adjustments is often precisely where women’s management appears most intensely.

The 2008 crisis affected families through multiple channels: work, income, credit, wealth, housing, and confidence. The Federal Reserve recorded, for the period from 2007 to 2010, a significant decline in real median income and a sharp reduction in median family wealth. When income and wealth shrink at the same time, the household loses both cash flow and the feeling of reserve. This pushes adaptation into the routine, because the family needs to find relief where some possibility of movement still exists.

This reorganization could begin almost invisibly. The weekly menu changed. Shopping became less frequent. Meal planning became more important. Children heard “not now” more often. Short trips were canceled. Repairs were postponed. Impulse purchases were watched. Leisure shifted into the home. The woman began remembering prices, comparing promotions, controlling supplies, and predicting what would run out before the end of the month.

None of this seems dramatic when observed separately. But together, it forms a new architecture of life. The home begins to operate in containment mode. Time also changes: cooking may require more planning; researching prices requires more attention; avoiding waste requires more work; replacing consumption with improvisation requires more energy. Financial savings often come with an increase in mental load and household labor.

This point is central to avoiding a superficial reading. Surviving a recession does not simply mean “spending less.” It means redesigning the routine so that lack does not disorganize everything at once. A family may save money, but spend more time. It may reduce purchases, but increase preparation, calculation, and effort. It may avoid debt, but live with permanent tension. It may keep the household functioning, but at the cost of almost constant vigilance.

This is where the article’s invisible pattern begins to appear with force: women’s management of scarcity as the invisible infrastructure of household survival. Infrastructure is not what appears first; it is what allows something to keep functioning. During the crisis, many women were that infrastructure. They did not eliminate vulnerability, but they managed it. They did not solve the economic collapse, but they absorbed part of its effects within family life.

The Pew Research Center observed that the Great Recession produced changes in Americans’ expectations and consumption and debt habits. This observation is important because it shows that the crisis did not change only indicators; it affected everyday behaviors. But, within the HMP reading, the next question is who had to operationalize that change inside the home. Often, that transition passed through women’s hands, attention, and fatigue.

The reorganization of routines also had a care dimension. It was not enough to cut. It was necessary to cut in a way that kept the family minimally integrated. A mother could reduce spending without telling children everything. A wife could postpone her own needs to preserve some emotional stability in the home. An adult daughter could help relatives, share purchases, or take on tasks to relieve costs. The routine was economic, but also affective.

For this reason, everyday life should not be treated as a secondary setting of the crisis. It was one of the fronts where the crisis was translated, absorbed, and partially contained. Major financial decisions mattered, but many families crossed the period through repeated small reorganizations: eating differently, shopping differently, getting around differently, caring differently, waiting differently.

This closure expands the value of everyday life. Because, in moments of collapse, financial survival depends less on isolated major moves and more on repeated, invisible, and emotionally costly microdecisions. And when this layer appears, the article stops being only about crisis and becomes about invisible competence.

The hidden story of 2008 is not only that families had to spend less. It is that many women had to engineer survival from inside the home, turning ordinary routines into a system of protection when the larger economy no longer felt reliable.

Chapter 2 — How making every dollar count became a household defense mechanism

How budgeting under crisis becomes less about planning and more about shielding the household

At first glance, saving money during the crisis may seem like simple restraint. But, in practice, it meant reorganizing food, transportation, shopping, priorities, care, and debt under continuous pressure. This shows that financial survival was also strategic work.

The central mechanism of this chapter is the change in the function of the budget. In stable times, the budget usually serves as a planning tool: it helps distribute income, organize goals, anticipate expenses, and, when possible, build some savings. During a deep crisis, however, it stops operating only as planning and begins to function as a shield. The goal is no longer only to make better decisions; it is to prevent external instability from dismantling domestic life from within.

The 2008 crisis intensified this process because it affected employment, income, housing, credit, and confidence at the same time. The Bureau of Labor Statistics recorded that the U.S. unemployment rate rose from 5.0% in December 2007 to 9.5% in June 2009, reaching 10.0% in October 2009, after the official end of the recession. This institutional data helps explain why many families began managing money with a sense of urgency, even before a complete loss of income occurred.

Inside the home, that urgency changes the budget’s question. The issue stops being “how much can we spend?” and becomes “what do we need to protect first?” Housing, food, energy, transportation, school, health, debt, insurance, and family care enter a kind of moral queue. Not everything can be maintained with the same intensity. Not everything can be cut without consequence. And, often, the person making that everyday triage is precisely the one who was already closest to the household routine.

This is where many women appear as invisible managers of household protection. Making every dollar count did not simply mean using coupons, switching brands, or spending less. It meant interpreting family risk in real time. If the husband’s job seemed threatened, if overtime disappeared, if credit became more expensive, if the home lost value, if a bill was late, the budget needed to react before the crisis became impossible to contain.

The difference is subtle, but decisive. Financial planning assumes some margin. Household defense emerges when the margin disappears. A woman who reorganized the shopping list, postponed a personal purchase, reduced travel, or cut small expenses was not merely being prudent. She was trying to create a barrier between the broader economic collapse and the minimum continuity of family life.

The Federal Reserve, in the Bricker et al. survey published in 2012 on family finances between 2007 and 2010, observed that real median family income before taxes fell by 7.7% during the period. The same study also recorded a steep decline in median family wealth, showing that the crisis reduced not only income flow but also the feeling of wealth protection. When income and wealth shrink together, the household budget begins to carry much greater responsibility.

This reading dialogues with feminist economics because it shows that the household budget is not a sphere separate from the economy. Diane Elson, in her work on productive and reproductive economics, argues that labor markets and family organization are interconnected through gender relations, care, and unpaid work. In 1999, Elson described labor markets as gendered institutions operating at the intersection between the productive economy and the reproductive economy. This perspective helps explain why a crisis in employment and credit quickly becomes pressure on those who manage the household’s everyday continuity.

For the real reader, this translates into a familiar situation: when money feels too short, each budget category begins to feel fragile. The grocery store becomes calculation. The credit card becomes a threat. The gas tank becomes a decision. The medical bill becomes an internal negotiation. The birthday gift becomes guilt. The small purchase stops being small because it begins to compete with everything that needs to keep functioning.

This pressure also prepares the ground for Article #90 — “The Hidden Price of Credit Card Debt for Women in America: How to Cut Interest, Escape Traps, and Build Financial Freedom”, because credit card debt can become a hidden survival trap when families use expensive credit to protect food, bills, and basic continuity during a crisis.

This reading also connects to Article #46 — “Household Debt and Economic Stability: Why Growth Alone Tells the Wrong Story”, because both show that economic stability cannot be measured only by overall growth. When the household needs to protect itself through constant cuts, the domestic economy reveals a fragility that broad indicators do not always make visible.

The cognitive point of this section is that a budget under crisis is not just a technique. It becomes a line of defense. During the 2008 crisis, many women were not simply “organizing expenses”; they were trying to prevent external instability from crossing fully into family life. The tight budget became a shield, and that shield required attention, renunciation, and everyday intelligence.

Why protecting essentials requires constant reprioritization in periods of scarcity

When scarcity sets in, protecting what is essential requires reordering priorities all the time. This is one of the most exhausting parts of household survival: the essential does not remain static. It changes as the bill arrives, the price rises, income fails, a child needs something, the car breaks down, debt comes due, or the family realizes the month is not over yet.

The mechanism here is continuous prioritization. In a comfortable budget, priorities can be defined in advance. In a compressed budget, they need to be reviewed repeatedly. What was possible in the first week of the month may become impossible by the third. What seemed optional may become urgent. What was important may be postponed because another problem has become more dangerous.

Academic literature on time, care, and household economics helps explain this dynamic. Aguiar, Hurst, and Karabarbounis, in a study published in the American Economic Review in 2013, analyzed time use during the Great Recession and observed that a relevant portion of lost paid work hours was absorbed by household production, including shopping, childcare, education, and health. This finding is important because it shows that the crisis did not merely remove income from the market; it also redistributed time and effort into the home.

In household life, this vigilance appears in repeated questions: what can wait? What cannot be late? What happens if this bill is left for later? Is it possible to replace one larger purchase with several smaller ones? Is it possible to reduce the expense without affecting the children? Is it better to pay the credit card or preserve money for food? Is it better to repair it now or hope it lasts another month?

These questions form a heavy cognitive load. They require calculation, but also emotional judgment. Often, women needed to decide not only what was financially necessary, but what was emotionally bearable. Cutting a personal expense could feel easier than cutting something for the children. Reducing family leisure could save money, but also increase the feeling of loss. Delaying personal care could protect the budget, but erode self-esteem and rest.

Nancy Folbre, in 2006, while discussing the care economy, argued that care needs to be measured and understood in a way that reveals gender differences in financial and time responsibility for dependents. This reading is valuable for the article because it shows that protecting essentials in a crisis does not involve only paying bills. It involves managing time, attention, care, dependency, and well-being within a smaller financial margin.

That is why financial survival during the crisis cannot be reduced to the idea of discipline. Discipline suggests linear control. Real scarcity produces constant negotiation. A woman may be organized, attentive, and careful, yet still live under pressure from difficult choices. The problem is not simply making good decisions; it is making decisions repeatedly within a field where no decision feels fully safe.

This process also reveals a moral dimension of money. In a crisis, every dollar gains a function. One dollar may protect food, transportation, medicine, school, debt, housing, or a small sense of normalcy. But the same dollar cannot protect everything at once. Making every dollar count, therefore, means choosing which part of life will be preserved first.

This choice was especially difficult because the 2008 crisis did not affect only the present. It corroded expectations. The Pew Research Center observed, in 2010, that the Great Recession altered many Americans’ expectations about retirement, home value, their children’s future, consumption, and financial recovery. This context indicates that families were not merely dealing with a difficult month. They were trying to reorganize priorities in an environment where the future seemed less reliable.

For many women, this uncertainty turned the budget into a practice of family protection. Protecting the essentials could mean keeping enough food, but also preserving some routine for the children. It could mean avoiding new debts, but also using credit when there was no other option. It could mean cutting visible expenses, but also silently absorbing personal losses to avoid tension inside the home.

The editorial risk here is romanticizing this capacity for adaptation. The article should not do that. Continuous reprioritization is not a sign that women “know how to make things work” by nature. It is a sign that the family and economic structure frequently transfers to them the work of transforming lack into continuity. They do not create the crisis, but they need to manage its effects at the most intimate level of daily life.

The closure of this analytical block is clear: protecting essentials during the crisis was not a single decision, made calmly and methodically. It was a sequence of repeated triage. Each new pressure required a new hierarchy. And, in that process, many women sustained the household not because scarcity became light, but because they learned to redistribute scarcity without letting life collapse all at once.

How women often turned routine financial restraint into a form of family stabilization

Routine financial restraint becomes family stabilization when it stops being only a reduction in spending and begins to organize the emotional and practical functioning of the home. This is the third movement of the chapter: showing that “making it stretch” did not only save money. Often, it helped preserve predictability, routine, and a minimum sense of control.

The mechanism is the conversion of restraint into continuity. The woman reduces, substitutes, postpones, and recalculates, but the final goal is not only to spend less. The goal is to keep the household operating. Someone still needs to think about meals, transportation, clothes, bills, school needs, birthdays, medications, the family’s emotional climate, and the small routines that prevent the crisis from feeling total.

This form of stabilization is difficult to see because it rarely appears as an event. It does not have a marked date like the collapse of a bank, the loss of a job, or a foreclosure. It happens in small, repeated, and almost silent decisions. Even so, these decisions produce real effects: they reduce waste, avoid delays, preserve priorities, hold conflicts in place, and maintain some order when the economic environment becomes unstable.

Bittman, England, Sayer, Folbre, and Matheson, in a 2003 study on the division of household labor, analyzed how income and gender interact in the distribution of household tasks. The study’s central conclusion is especially useful here: even when women’s economic contribution increases, gender continues to weigh heavily in the division of household labor. This helps explain why, in a crisis, responsibility for everyday stabilization tends to fall on women even when they also participate in the labor market.

The BLS described the 2007–2009 recession as a period of sharp deterioration in the labor market, with a significant increase in unemployment and a decline in job security. This information matters because job insecurity affects not only those who lose work. It changes the behavior of entire families. Even when income still exists, the fear of losing it can turn restraint into a strategy of anticipatory stabilization.

In this environment, women often began acting as household shock absorbers. If there was less money, they reorganized the routine. If there was fear, they tried to maintain normalcy. If there was debt, they negotiated priorities. If there were children, they measured how much of the crisis would be visible to them. If there was marital or family tension, they often mediated conversations, hid their own anxiety, or turned worry into practical action.

Routine restraint could appear as a sequence of simple gestures: cooking more at home, comparing prices, reducing waste, planning purchases, using the car less, canceling subscriptions, reusing materials, switching brands, suspending small luxuries, finding free leisure alternatives, postponing personal purchases. But the structural reading is deeper. These gestures functioned as an architecture of resistance. They helped the home remain recognizable despite the crisis.

The Federal Reserve showed that, between 2007 and 2010, families lost real median income and median wealth, reducing the safety margin of many households. When that margin shrinks, stabilizing family life requires turning small habits into a system. It is not enough to cut once. The cut must be maintained, adjusted when it stops working, replaced when the replacement fails, and reorganized when another problem appears.

This repetition creates a form of invisible labor. The family may perceive that there is food on the table, bills are minimally organized, and the routine is preserved, but it may not see the effort behind it. It may not see the price comparisons, the anxiety before opening the statement, the calculation before filling the gas tank, the discomfort of saying “no,” the guilt of postponing something necessary, or the fatigue of turning restraint into normalcy.

Arlie Hochschild and Anne Machung, in The Second Shift from 1989, helped consolidate the idea that many women face a second shift of household and care work after paid employment. This sociological lens is important for understanding the 2008 crisis because financial restraint did not replace that work; it was added to it. The woman who made the money stretch often also continued cooking, caring, mediating conflicts, organizing the home, and holding the family’s emotional routine together.

Here, the expression domestic strategy gains strength. Domestic strategy is not lesser than formal financial strategy; it is simply less recognized. During the 2008 crisis, many women did not have access to major economic levers. They did not control interest rates, banks, public policies, or housing markets. But they controlled, as much as possible, how scarcity entered the home. This limited, repeated, and tiring control helped many families get through the period.

This reading also connects to Article #47 — “Consumer Spending, Well-Being, and Sustainability: The Everyday Choices That Shape the Economy”, because it shows that consumption choices are not merely individual preferences. In moments of crisis, they reveal well-being, fear, adaptation, and the capacity for household support. Everyday consumption becomes a thermometer of family stability.

Family stabilization, however, does not eliminate vulnerability. This point needs to remain clear. Women could make the money stretch, but that did not mean the crisis was resolved. They could keep the household functioning, but that did not erase income loss, debt, fear, or insecurity. They could preserve routine, but often at the cost of emotional strain and personal renunciation.

The cognitive closure of this movement of the chapter is this: making every dollar count became a household defense mechanism because, during the crisis, money needed to protect more than purchases. It needed to protect continuity. And, in many homes, it was women who turned financial restraint into minimum stability, sustaining the family through small, exhausting, and deeply strategic choices.

Chapter 3 — What women began to manage beyond money

Why money management in crisis also becomes emotional and logistical management

When a crisis enters the household budget, it rarely remains only in the realm of numbers. Money remains central, but it begins to carry other functions: organizing the routine, protecting children, reducing conflicts, preserving some predictability, and managing the collective fear inside the home. This is the main mechanism of this movement of the chapter: in periods of scarcity, financial management expands into emotional and logistical management.

During the 2008 crisis, many women were not only asking how much was available for food, transportation, or bills. They also needed to decide how to communicate the lack, how to maintain their children’s routine, how to prevent financial anxiety from contaminating every space in the home, and how to adapt daily life without letting the family feel that everything had lost stability. The budget, in this context, became a language of care.

Nancy Folbre, in 2006, while discussing the care economy, argued that care needs to be measured in a way capable of revealing gender differences in financial and time responsibility for dependents. This reading is essential to Article #57 because it shows that managing scarcity does not involve only available money, but also time, attention, dependency, protection, and emotional responsibility.

In practice, this means that the woman who reorganized the budget during the crisis could also be reorganizing meals, transportation, schedules, family conversations, children’s expectations, and consumption decisions. The cut expense was only the visible part. Behind it was a sequence of less visible questions: how to cut without frightening? How to postpone without creating conflict? How to say “no” without transmitting despair? How to protect the family when her own sense of security was already shaken?

This type of management requires constant reading of the household environment. The crisis does not affect all family members in the same way. Children may feel changes without understanding the cause. Partners may respond with silence, irritation, or shame. Relatives may need help. The woman who already occupied the center of household organization often became the emotional interpreter of the crisis as well. She read signals, anticipated tensions, and tried to convert scarcity into a bearable routine.

The literature on invisible household labor helps name this layer. Arlie Hochschild and Anne Machung, in The Second Shift, originally published in 1989, consolidated the idea that many women perform a second shift of household and care work after paid employment. This sociological lens helps explain why, in a crisis, financial management does not replace previous household work; it is added to it.

The point is decisive: when the budget shrinks, the home does not automatically become simpler. Often, it becomes more labor-intensive. Saving money may require more cooking, more research, more planning, more negotiation, more reuse, and more explanation. The reduction in spending may come with an increase in time, attention, and effort. Thus, the crisis produces a silent exchange: less money circulating, more invisible work needed to keep life functioning.

The 2008 crisis intensified this pattern because it affected income, employment, housing, and confidence at the same time. The Bureau of Labor Statistics recorded that the U.S. unemployment rate rose sharply during the recession, reaching 10.0% in October 2009. This scenario amplified the sense of threat even within families that had not yet fully lost income, because job insecurity began to shape household decisions before the worst actually happened.

For the real reader, this appears as a very concrete feeling: it is not enough to pay the bill; the atmosphere of the home must be preserved. It is not enough to cut the expense; it is necessary to decide who will feel the cut. It is not enough to buy less; it is necessary to turn less into enough. Financial management also becomes management of expectations, emotions, and daily logistics.

This is where the article distances itself from a superficial view of “crisis budgeting.” A budget in crisis is not just a tight spreadsheet. It is a practice of mediation. The woman who manages scarcity needs to translate numbers into meals, bills, transportation, conversations, renunciations, and small forms of protection. Money is the starting point, but survival requires managing everything that money sustains.

The cognitive closure of this section is clear: during the 2008 crisis, many women began managing much more than money. They managed the emotional and logistical impact of scarcity, trying to keep the home functional when the broader economy had already lost stability. This is one of the reasons why making every dollar count needs to be understood as economic and emotional labor at the same time.

How women absorbed the hidden coordination work behind family survival

The second movement of the chapter deepens the idea of invisible coordination. In a crisis, survival does not depend only on isolated spending cuts. It depends on coordinating many parts of life at the same time: food, transportation, care, schedules, bills, debts, school, health, work, fear, and expectations. The mechanism here is the transformation of survival into continuous coordination work.

This work is often difficult to recognize because it does not appear as a single task. No one says, “today I am going to coordinate the economic survival of the household.” But that is exactly what many women do when they compare prices, change menus, reorganize bills, tell children about limits, avoid waste, negotiate priorities, and maintain the minimum functioning of the routine.

Aguiar, Hurst, and Karabarbounis, in a study published in the American Economic Review in 2013, analyzed time use during the Great Recession and observed that part of the hours lost in paid work was absorbed by household production, including activities such as shopping, childcare, education, and health. This academic data is important because it reveals that the crisis did not merely remove income from the market; it shifted effort into the home.

This shift helps explain why household survival can seem invisible. When a family reduces expenses, the result may be perceived as “we spent less.” But the real process may have required more work: planning meals, researching discounts, caring for children at home, solving problems without hiring help, replacing paid services with household time, and turning consumption into internal production.

For many women, this coordination work was even more intense because it rested on responsibilities that already existed. Before the crisis, they may already have been the main people responsible for remembering what was missing, following the children’s routine, organizing shopping, preparing meals, and noticing when something was out of place. During the recession, these tasks gained another pressure: now they had to be done with less margin, less money, and more fear.

The crisis transformed the everyday question. It was not only “what do we need to buy?” It was “how do we make this fit without compromising the rest?” It was not only “what are we going to eat?” It was “how do we maintain enough food without increasing the bill?” It was not only “how do we take the children?” It was “how do we reduce cost, time, and tension at the same time?” The woman who answered these questions was not merely performing tasks. She was connecting fragile parts of a pressured household system.

This layer comes directly close to Article #51 — “The Double Shift: How Women Balanced Survival Jobs and Family During the 2008 Financial Crisis”, but with an important difference. Article #51 deepens the double shift between work, care, and survival. This article shows how the very management of scarcity inside the home became an invisible infrastructure, even when there was no formal change in employment or paid work hours.

Coordination also involved protecting the family from symbolic ruptures. Maintaining a meal around the table, preserving a school routine, finding free leisure, celebrating dates more simply, or preventing children from perceiving all the economic fear were forms of stabilization. They did not eliminate the crisis, but they prevented scarcity from immediately turning into emotional disorganization.

The literature on care helps support this reading. Folbre, in 2006, highlighted that responsibility for care involves financial and time dimensions that often do not appear in traditional economic measures. When applied to the 2008 crisis, this idea shows that women could be producing family stability without that effort being recorded as income, formal productivity, or visible economic recovery.

This invisibility is an essential part of the article’s pattern. The family may continue functioning, and precisely because of that, the work behind continuity disappears. If there is food, clean clothing, a prioritized bill, a cared-for child, and a minimum routine, the result seems natural. But what seems natural may have been produced through repeated decisions, mental calculation, and emotional strain.

The expression “hidden coordination work” is useful because it reveals what remains hidden between one financial decision and another. Survival does not arise only from the final cut, but from the connection among several choices. Cutting a subscription may help a bill. Cooking at home may reduce spending, but increase work. Avoiding transportation may save money, but require schedule reorganization. Each decision creates another. Coordinating that chain is work.

The cognitive closure of this block is that family survival during the 2008 crisis depended on a coordination that rarely appeared in official narratives of the recession. Many women absorbed this work because they were already positioned at the center of the household routine. They transformed scattered decisions into minimum continuity, stitching together a home pressured from within while the economy failed from the outside.

Why continuity itself becomes something women must actively produce under scarcity

The third part of the chapter consolidates a decisive idea: in times of scarcity, continuity is not automatic. It needs to be produced. The home does not keep functioning simply because its members want stability. It keeps functioning because someone reorganizes resources, adjusts expectations, manages conflicts, anticipates needs, and turns lack into a possible routine.

The mechanism here is the active production of continuity. In normal periods, certain routines seem given: meals, school, bills, transportation, small family rituals, basic care, birthdays, essential purchases. In periods of crisis, these routines begin to require extra work. What once flowed with some predictability needs to be rebuilt every day.

During the Great Recession, this effort became heavier because many families lost income, wealth, and confidence at the same time. The Federal Reserve, in the Bricker et al. study published in 2012, recorded that real median family income fell between 2007 and 2010, while median family wealth suffered an even deeper decline. This context helps explain why so many families needed to produce everyday stability from a weakened material base.

Producing continuity meant preventing the crisis from invading every gesture of life. Sometimes, this involved making a simple meal seem sufficient. Sometimes, it meant explaining a postponed purchase as a temporary choice, not as collapse. Sometimes, it meant preserving the children’s routine even when the adults were frightened. Sometimes, it meant hiding one’s own worry so the home would not live in a permanent state of alarm.

This production of continuity had a cost. It required financial vigilance, emotional energy, and the ability to improvise. The woman could be tired, worried, or insecure, yet still needed to maintain some order. When the home depends on someone to transform uncertainty into functioning, that person becomes part of the family’s emotional infrastructure.

Arlie Hochschild and Anne Machung, in 1989, helped make visible women’s overload in household organization and everyday care. This contribution is important here because the 2008 crisis did not create household inequality from scratch; it intensified previous structures. Women who already carried a significant part of the routine also began carrying the task of preserving continuity under scarcity.

Continuity also had a very concrete practical dimension. If the family could not eat out, someone needed to plan more meals. If it could not pay for certain services, someone needed to do more at home. If the child needed something for school, someone needed to find an alternative. If the budget did not close, someone needed to reorganize priorities. If tension rose, someone needed to mediate.

This sequence shows that the household economy is not only consumption. It is also the production of everyday life. The home produces meals, care, rest, belonging, predictability, and meaning. When money decreases, this production does not disappear. It simply requires more unpaid work, more creativity, and more renunciation.

Research on the effects of the Great Recession also helps show that the impact of the crisis was not restricted to the financial balance sheet. Bourassa and colleagues, in a study published in 2021, analyzed financial stressors during the Great Recession and associated this type of pressure with later effects on health and well-being. Although this study looks at broad consequences, it reinforces a central idea for this article: prolonged financial pressure seeps into everyday life and into the emotional body of families.

That is why family continuity cannot be treated as a sign that “everything worked out.” Many families continued functioning, but that continuity was precarious, exhausting, and sustained by invisible effort. The set table did not mean absence of fear. The preserved school routine did not mean financial calm. The budget closed at the limit did not mean security. It meant that someone managed to hold the structure together for one more day, one more week, one more month.

This is the narrative strength of the invisible pattern in Article #57. Women’s management of scarcity as the invisible infrastructure of household survival appears precisely when continuity seems natural, but was produced under pressure. The woman does not merely manage money; she manages the passage between external collapse and possible internal life.

The cognitive closure of the chapter is this: during the 2008 crisis, many women began managing beyond money because survival required more than paying bills. It required producing continuity. And producing continuity under scarcity meant turning care, logistics, emotion, and budget into an everyday engineering of minimum stability.

Chapter 4 — How scarcity became invisible survival labor

How repeated cutbacks become a form of unpaid labor during economic crisis

When scarcity is prolonged, cutting expenses stops being a one-time decision and becomes a routine of labor. This is the central mechanism of this movement of the chapter: in an economic crisis, repeated cuts do not only reduce expenses; they transfer effort into the home, especially to whoever needs to reorganize everyday life with fewer resources.

During the 2008 crisis, many families did not face only one tight month. They faced a sequence of months marked by unemployment, reduced income, fear of losing the home, more restricted credit, and falling confidence. The Bureau of Labor Statistics, in its 2012 analysis of the 2007–2009 recession, recorded that unemployment in the United States rose from 5.0% in December 2007 to 10.0% in October 2009. This data helps contextualize why household management needed to change in intensity: it was not just a passing phase of prudence, but a prolonged environment of economic threat.

Inside the home, that threat translated into tasks. Cutting expenses could mean cooking more, planning meals in advance, looking for promotions, comparing prices in different stores, reusing leftovers, repairing instead of replacing, canceling services, reducing transportation, postponing purchases, and negotiating family priorities. The money saved appeared as the result, but the work required to produce that saving often disappeared from the narrative.

This invisibility is decisive. When a family spends less on eating out, someone needs to take on more household food preparation. When it cuts paid services, someone needs to replace that service with time and energy. When it reduces purchases, someone needs to control supplies, anticipate needs, and avoid waste. When it postpones expenses, someone needs to manage the risk that the problem will become bigger later. Thus, financial savings may be accompanied by an increase in unpaid labor.

Economist Nancy Folbre, in 2006, while discussing the measurement of the care economy, argued that care and unpaid work need to be analyzed because they sustain economic life without fully appearing in traditional metrics. This perspective is essential for understanding Article #57: during a crisis, part of the economic shock is absorbed by extra household labor, often female, that does not enter as income, does not appear as employment, and rarely receives proportional recognition.

This point also dialogues with Aguiar, Hurst, and Karabarbounis, who in 2013 analyzed time use during the Great Recession in the American Economic Review. The study showed that part of the time freed by reduced paid work was shifted to household production, including shopping, care, education, health, and other activities inside the home. The HMP reading adds one layer: even when that shift was not formally planned, it required everyday coordination, and many women were pushed into the center of this reorganization.

In real life, this appears in small scenes. The woman who replaces ready-made meals with food cooked at home may save money, but gains more work. The woman who researches deals before buying may reduce spending, but loses time and mental energy. The woman who cancels a paid activity for the children may need to create another way to occupy, explain, and compensate. The woman who holds back a personal purchase may protect the budget, but pays with silent renunciation.

That is why repeated cutting cannot be treated as a simple rational choice. It is a form of unpaid labor when it requires planning, execution, monitoring, and continuous adaptation. The cut does not end when the expense disappears. It continues in the effort to reorganize the routine so that the absence of that expense does not dismantle family life.

This reading connects directly to Article #51 — “The Double Shift: How Women Balanced Survival Jobs and Family During the 2008 Financial Crisis”. While Article #51 shows the double shift between paid work and care, Article #57 reveals a complementary layer: even seemingly simple household cuts could create a new invisible shift of planning, substitution, and restraint.

The cognitive closure of this section is that cutting expenses during the 2008 crisis was not only spending less. It was working more to make less money sustain more needs. And, in many homes, this extra work was performed by women who transformed restriction into continuity, without this everyday engineering being recognized as a real part of economic survival.

Why scarcity intensifies mental load rather than simply reducing spending

Scarcity does not only reduce consumption. It increases mental load. This is the main mechanism of this analytical block: when money becomes short, the family may spend less, but someone needs to think more, anticipate more, compare more, calculate more, and manage more risks at the same time.

The idea of mental load is important because it shows that the crisis does not happen only when a bill is paid or left for later. It happens before, during, and after the decision. Before, when the woman tries to anticipate what is still coming. During, when she needs to choose between competing priorities. After, when she carries doubt about whether she made the right choice.

During the 2008 crisis, this mental load was intensified by an environment of broad uncertainty. The Federal Reserve, in the Bricker and colleagues study published in 2012 on U.S. family finances between 2007 and 2010, recorded a 7.7% decline in real median family income before taxes and a much deeper reduction in median wealth. When income and wealth fall at the same time, the feeling of protection decreases. The family does not lose only available money; it also loses confidence in its own ability to absorb shocks.

For the woman managing everyday life, this loss of margin changes the way she thinks. She does not look only at the current balance. She thinks about rent or the mortgage, food until the end of the month, fuel, school, medications, the credit card bill, a possible car repair, the chance of a layoff, the child who needs clothes, the relative who may ask for help. The budget becomes a map of simultaneous threats.

Arlie Hochschild and Anne Machung, in The Second Shift from 1989, helped make visible how many women accumulate paid work with a second domestic and emotional shift. Although the book predates the 2008 crisis, its sociological lens helps understand what the recession intensified: when the economy tightens, the second shift not only continues; it gains an additional layer of financial vigilance.

This vigilance is different from organization. Organization can be planned. Vigilance is born from the fear that any mistake will have a greater consequence. The woman does not only organize the shopping list; she imagines what will happen if the price is higher. She does not only decide to pay a bill; she calculates which delay would cause less damage. She does not only avoid a purchase; she tries to measure whether the renunciation will affect the family in another way. Scarcity turns thinking into constant monitoring.

In practice, this produces exhaustion. One thing is knowing that it is necessary to spend less. Another is living with the permanent obligation to turn every purchase into a judgment. The grocery store stops being an ordinary task and becomes a sequence of decisions. The credit card stops being a tool and becomes a risk. The family outing stops being rest and becomes calculation. Rest, often, also begins to require justification.

Economic psychology helps interpret this effect. Sendhil Mullainathan and Eldar Shafir, in Scarcity, published in 2013, argued that scarcity captures attention and reduces the mental bandwidth available for other decisions. Although the book addresses scarcity in several contexts, its contribution is useful for this analysis: when lack occupies the mind, managing life requires more cognitive effort, not less. A person may seem indecisive or excessively worried, but often she is simply trying to operate within a compressed mental margin.

This reading is especially important to avoid individual blame. The woman who repeats calculations, hesitates before a small purchase, or feels anxiety when opening a bill is not necessarily being “dramatic” or “disorganized.” She may be responding to a structure of scarcity that has turned simple decisions into loaded decisions.

Mental load also had a relational dimension. The woman might need to decide what to tell and what to soften. She might try to protect the children from the feeling of crisis. She might avoid conversations so as not to increase conflict. She might absorb the worries of a partner or the extended family. She might turn fear into practical action because someone needed to keep the routine functioning. This is not only financial management. It is emotional management of instability.

The Institute for Women’s Policy Research, in a 2010 report on economic insecurity after the Great Recession, indicated that women and men faced significant concerns about employment, income, savings, and the ability to deal with unforeseen events. From the perspective of this article, the central point is that this insecurity did not remain outside the home. It was translated into household vigilance, and that vigilance often accumulated on women who were already responsible for care, shopping, and organizing the routine.

The cognitive closure of this movement of the chapter is that scarcity does not merely reduce expenses. It increases the mental work required to make life fit inside what remains. During the 2008 crisis, many women carried this load in silence, transforming permanent calculation into an invisible form of family survival.

How women turned improvisation, substitution, and restraint into survival infrastructure

The third part of the chapter shows how improvisation, substitution, and restraint became survival infrastructure. The mechanism here is the organized repetition of adaptation: when a family loses margin, small solutions need to stop being exceptions and become a system.

Improvising in a crisis does not mean acting without method. Often, it means finding possible solutions when ideal solutions have become out of reach. Substituting is not only replacing an expensive brand with a cheaper one. It can mean replacing a paid service with household labor, an outside activity with a free alternative, a new purchase with a repair, a planned meal with reused leftovers, a previous routine with one that is cheaper and more labor-intensive.

During the 2008 crisis, this adaptation became part of daily life for many families. The Pew Research Center, in 2010, observed that the Great Recession altered consumption habits, expectations about the future, perceptions of security, and family decisions. The idea of “new frugality” identified in that context helps explain the broader social environment, but Article #57 needs to go beyond the phrase. The point is not only that families became more frugal; it is that someone needed to operationalize that frugality within the routine.

This operationalization frequently passed through women. They transformed substitutions into continuity. If the family could no longer buy as before, it was necessary to discover what still worked. If paid leisure disappeared, it was necessary to invent another kind. If food needed to stretch further, menus had to be planned. If a purchase was postponed, frustration had to be managed. If a service was cut, the task had to be absorbed.

Diane Elson, in 1999, while analyzing labor markets as gendered institutions, showed how the productive economy and the reproductive economy are connected. This contribution helps illuminate the 2008 crisis because the shock in the labor market was not limited to formal employment. It pressured the reproductive economy of the home: care, food, organization, cleaning, routine, rest, emotional protection, and maintenance of daily life.

The expression “survival infrastructure” is useful because infrastructure is what sustains functioning, even when it does not draw attention. During the crisis, repeated household improvisations functioned as this silent foundation. A cheaper meal, in isolation, does not change economic history. But thousands of similar decisions, repeated inside millions of homes, show how part of the macroeconomic shock was absorbed by family micromanagement.

This point also connects to Article #47 — “Consumer Spending, Well-Being, and Sustainability: The Everyday Choices That Shape the Economy”. Everyday consumption is not merely an expression of preference. In a crisis, it becomes a thermometer of pressure and adaptation. When families substitute, cut, and improvise, they are responding to economic conditions that cross into the home.

Restraint, however, should not be confused with a full solution. Women could improvise with competence and still live with vulnerability. They could substitute products and still feel a loss of quality of life. They could cut expenses and still accumulate anxiety. They could protect children from part of the impact and still absorb the emotional weight of the crisis. The infrastructure of survival was real, but precarious.

This tension is essential to the HMP reading. The article needs to value practical intelligence without romanticizing lack. Improvising may reveal creativity, but it also reveals absence of margin. Substitution may show adaptation, but it also shows restriction. Restraint can protect, but it also wears people down. Women’s competence should not be used to erase the injustice of overload.

In household life, the infrastructure of survival could form in layers. First came substitution: switching brands, services, habits. Then came reorganization: changing schedules, routines, menus, transportation. Next came emotional restraint: explaining less, softening more, protecting children, avoiding conflict. Finally came repetition: doing it all again the following month, with new pressures and little guarantee of relief.

This is where scarcity becomes invisible survival labor. What appears to be spontaneous improvisation is often a system of microdecisions. What appears to be simple saving is coordination. What appears to be household restraint is structural protection of family life in a scenario of instability.

The cognitive closure of the chapter is that, during the 2008 crisis, many women transformed improvisation, substitution, and restriction into a domestic architecture of resistance. They did not control the recession, the banks, the housing market, or unemployment. But, inside the home, they converted insufficient resources into provisional continuity. This was the invisible force of survival: not eliminating scarcity, but preventing it from destroying everything at once.

Chapter 5 — Why women became central to the everyday engineering of the crisis

Why caregiving roles made women more likely to manage scarcity from the inside

Women’s centrality in managing scarcity during the 2008 crisis did not come from nowhere. It grew out of a previous structure: in many families, women were already primarily responsible for organizing care, food, shopping, routines, children’s needs, household schedules, and small adjustments in everyday life. When the crisis arrived, this practical position inside the home pushed them into the center of managing lack.

The mechanism here is direct: whoever already manages the routine is usually the first person to notice where scarcity begins to tighten. The woman notices when the food supply needs to last longer, when the price has gone up, when the child needs something for school, when the bill does not fit into the month, when an expense needs to be postponed, and when the household begins to lose predictability. In a crisis, this everyday sensitivity becomes an economic function.

Nancy Folbre, in 2006, while discussing the care economy, argued that care work needs to be measured because it sustains dependents, families, and social systems without fully appearing in traditional economic metrics. This reading helps explain why women became central to the everyday engineering of the crisis: they were not simply “helping” the household. They were managing an essential part of the daily reproduction of family life.

During the 2008 crisis, this responsibility gained another intensity. The recession pressured income, employment, housing, credit, and expectations. But the impact of these shocks had to be translated into concrete decisions inside the home. If there was less money, someone had to decide how to reorganize meals. If there was fear of unemployment, someone had to reduce expenses before income disappeared. If credit became more dangerous, someone had to think about how to avoid new debt. If children noticed changes, someone had to explain without frightening them.

That is why care cannot be treated as a subject separate from the economy. Caring, in times of crisis, also means calculating. It means transforming limited resources into food, transportation, routine, emotional protection, and continuity. The woman who decides how to make food stretch, how to keep a child protected from family anxiety, or how to cut expenses without completely dismantling the routine is exercising a form of everyday economic management.

Diane Elson, in 1999, while analyzing labor markets as gendered institutions, showed that the productive economy and the reproductive economy are connected. This perspective is essential to Article #57 because the 2008 crisis did not affect only formal employment or financial markets. It pressured the reproductive economy of the home: care, food, cleaning, transportation, emotional maintenance, and the organization of ordinary life.

For the real reader, this connection appears in a very concrete way. When money tightens, the work of “making it fit” is usually not abstract. It lives in the grocery list, the lunchbox, the electricity bill, the gas tank, the medicine, the clothing that needs to last longer, the reused meal, the simplified birthday, the choice between paying a debt or preserving money for food. These gestures seem domestic, but they carry an economic function.

This centrality, however, should not be romanticized. Women did not become managers of scarcity because they were born more prepared to suffer or improvise. They became central because social structures had already placed them close to care and household organization. The crisis only intensified an inequality that already existed.

This point connects Article #57 to Article #51 — “The Double Shift: How Women Balanced Survival Jobs and Family During the 2008 Financial Crisis”. While Article #51 deepens the double shift between paid work and care, this chapter shows how caregiving roles also placed women at the center of the internal management of scarcity. The crisis did not create women’s overload; it increased its urgency.

The cognitive closure of this section is that women became central to the everyday engineering of the crisis because they were already positioned where the crisis became concrete: inside the routine. When the broader economy failed, the household needed to be reorganized from within. And, in many families, those who had already sustained care also began sustaining the daily translation of scarcity.

How gendered domestic expectations turned women into crisis managers by default

The second layer of this chapter shows that women’s management of the crisis was not merely the result of individual skill. It was also a consequence of gendered domestic expectations. In many families, even when women worked outside the home, they were still expected to notice, organize, and solve much of the household’s practical needs. During the crisis, these expectations turned women into managers of scarcity by default.

The mechanism is the naturalization of responsibility. When a task is seen as “women’s work,” it stops appearing as work and begins to seem like a personal trait. The woman who remembers what is missing, compares prices, reorganizes meals, controls bills, calms children, and adapts the routine may be seen as careful, organized, or strong. But, in the context of crisis, that “organization” is real economic labor.

Arlie Hochschild and Anne Machung, in The Second Shift from 1989, helped consolidate the idea that many women face a second shift of household and care work after paid employment. This lens is important because it shows that, when the 2008 crisis increased pressure on the household, it did not fall on a neutral domestic division. It fell on an arrangement in which women already carried much of the everyday coordination.

Bittman, England, Sayer, Folbre, and Matheson, in a study published in 2003, analyzed income, gender, and the division of household labor. The study showed that, even when women contribute economically, gender continues to weigh on the distribution of household tasks. This evidence helps explain why, during a recession, responsibility for adjusting domestic life often remained female, even in households where the woman also participated in the labor market.

In practice, this means that the woman could be worried about her own job, family income, debt, and the future while, at the same time, remaining responsible for keeping the household functioning. The crisis did not replace her previous tasks. It added a new layer: turning lack into a possible routine.

This transformation could be silent. If the family needed to spend less, she looked for alternatives. If food needed to stretch, she reorganized the menu. If paid leisure disappeared, she tried to create another kind of distraction. If the children asked why something had changed, she found an explanation. If her partner was anxious or ashamed because of lost income, she could absorb part of the emotional climate. All of this formed a crisis management system that rarely received that name.

The problem is that, when this work is naturalized, it becomes invisible. The family notices that the routine continues, but does not see the effort of continuity. It notices there is food, but not the calculation. It notices bills were prioritized, but not the anxiety. It notices the children remain protected, but not the emotional mediation. The woman appears as someone who “handles it,” when in fact she is operating a system of containment.

The Institute for Women’s Policy Research, in 2010, while analyzing economic insecurity in the period after the Great Recession, pointed to significant concerns among women about employment, income, savings, debt, and the ability to deal with emergencies. Within the logic of this article, this type of insecurity needs to be read alongside the domestic burden: women were not only exposed to the crisis as individuals; many were also responsible for managing how the crisis would be felt by everyone inside the home.

This reading prevents a dangerous conclusion: that women were central because they were naturally better at household economics. The point is different. They were central because social expectations had already positioned them as responsible for maintaining everyday life. The crisis only made that responsibility heavier, more urgent, and harder to ignore.

This layer also connects to Article #46 — “Household Debt and Economic Stability: Why Growth Alone Tells the Wrong Story”, because debt and household stability are not only numbers. They are lived by people who need to decide which bills to prioritize, which risks to accept, and which sacrifices to absorb. When this management falls unequally on women, the household economy reveals an inequality that aggregate indicators can hide.

The cognitive closure of this block is that women became crisis managers by default not because the crisis chose women, but because the home had already been socially organized to depend on them. The expectation that they would care, anticipate, adjust, and maintain the routine turned scarcity into yet another female responsibility. And that responsibility, during the 2008 crisis, was an intense form of invisible labor.

Why invisible household stabilization is a gendered response to economic instability

The third part of the chapter consolidates the thesis: the invisible stabilization of the home during the crisis was a gendered response to economic instability. This means that, when larger systems failed, employment, credit, housing, confidence, part of the impact was absorbed by domestic practices of restraint, care, and reorganization. And these practices often fell on women.

The mechanism is the household absorption of the macroeconomic shock. The crisis happens in markets, banks, companies, and public policies, but its effects need to be managed inside the home. When income falls, someone reorganizes expenses. When credit tightens, someone avoids new debt. When the future seems uncertain, someone reduces everyday risks. When the family feels fear, someone tries to preserve routine. This passage from macro to micro is one of the keys of Article #57.

The Federal Reserve, in the Bricker and colleagues survey published in 2012 on family finances between 2007 and 2010, recorded a decline in real median income and a significant loss of median wealth among U.S. families. These data show the size of the material compression. But they do not fully capture the internal work required to transform that compression into everyday survival.

This is the space where invisible household stabilization enters. It appears when a woman turns a smaller budget into possible meals, when she replaces consumption with improvisation, when she reorganizes bills, when she protects children from part of the fear, when she absorbs anxiety to avoid emotional collapse, when she makes difficult choices seem manageable. The family may continue functioning, but that continuity is not neutral. It is produced.