The Psychology of Impulse Spending: Triggers That Drive Emotional Buying and Regret

Editorial Introduction

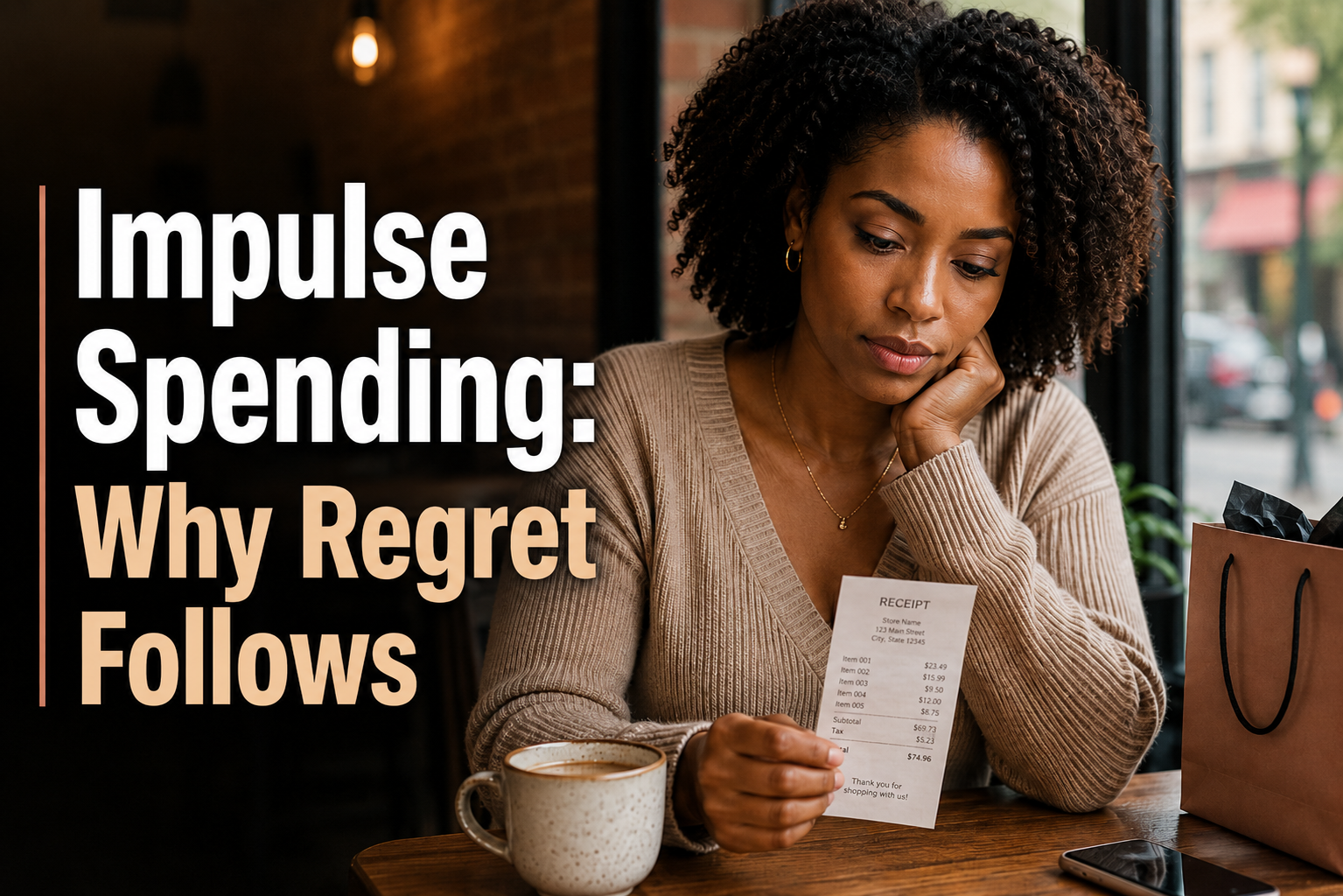

Impulse spending often feels like a small decision in the moment. A quick order, a discounted item, a late-night purchase, or a cart that suddenly becomes impossible to ignore can all feel harmless while the emotional pressure is active. For a few minutes, buying may feel like relief, reward, or control. The regret usually arrives later, when the emotional charge fades and the cost becomes real.

That is why impulse spending is not simply about weak self-control. It is shaped by emotional triggers, stress, mental fatigue, digital convenience, urgency cues, personalized offers, and payment systems that make spending feel almost invisible. The purchase may look spontaneous, but the decision is often prepared before the buyer fully realizes it.

This article examines the psychology of impulse spending through a behavioral, emotional, and structural lens. Instead of asking why someone “failed” to resist a purchase, it asks what conditions made the purchase feel natural, urgent, comforting, justified, or difficult to pause at that specific moment.

The analysis moves through the hidden triggers that activate emotional buying, the role of stress and mental overload, the immediate reward of purchasing, the acceleration created by digital environments, and the reason regret usually appears after the purchase rather than before it.

The article also distinguishes impulsive, emotional, and compulsive consumption, avoiding simplistic labels. Its purpose is not to moralize spending, but to make visible the mechanisms that shape everyday financial decisions and help readers understand impulse without guilt.

Editorial distinction: This article focuses on the moment before impulse spending feels like a conscious decision. While broader articles on emotional spending explain why money choices feel personal, this analysis maps the specific triggers that make buying feel immediate, justified, and difficult to pause. In the HerMoneyPath ecosystem, Article #23 functions as the behavioral trigger map of Cluster 2, explaining how impulse spending begins before regret becomes visible.

Quick Answer

Impulse spending usually happens when emotional pressure, stress, digital convenience, urgency cues, and reduced payment friction make buying feel easier than pausing. The purchase may seem spontaneous, but many triggers often prepare the decision before conscious reflection begins. Regret usually appears later, when the emotional relief fades and the financial cost becomes clearer.

Key Insights

- Impulse spending often begins before the buyer fully recognizes the decision. Emotional pressure, digital cues, urgency messages, and reduced friction can quietly prepare the purchase before conscious reflection has time to intervene.

- Emotional buying is not simply a failure of self-control. Stress, mental fatigue, overload, and the search for relief can make buying feel like a quick way to regain comfort, reward, or control in the moment.

- The pleasure of buying usually arrives before the real cost becomes visible. Digital payments, saved cards, credit, and one-click checkout can separate the emotional reward of purchasing from the later financial consequences.

- Regret often appears after the purchase because the emotional state has changed. What felt urgent, comforting, or justified during the impulse may look unnecessary once the emotional charge fades and the budget impact becomes clearer.

- Digital environments accelerate impulse spending by removing natural pauses. Personalized offers, notifications, limited-time prompts, and frictionless checkout shorten the space between desire and action.

- Impulse spending, emotional spending, and compulsive consumption are not the same thing. This article focuses on the triggers that make buying feel immediate and difficult to pause, without reducing every unplanned purchase to a disorder or moral failure.

- The long-term impact of impulse spending is usually cumulative. A single purchase may seem harmless, but repeated small decisions can quietly affect savings, credit card balances, financial confidence, and emotional well-being over time.

Table of Contents

- Editorial Introduction

- Chapter 1 — Why impulse spending begins with emotional triggers

- Chapter 2 — Invisible triggers: how everyday stimuli anticipate the purchase decision

- Chapter 3 — The role of stress, mental fatigue, and emotional overload

- Chapter 4 — Immediate reward and psychological relief in the act of buying

- Chapter 5 — Digital environments, reduced friction, and the acceleration of impulse

- Chapter 6 — Why regret emerges after, not before, the purchase

- Chapter 7 — The difference between impulsive, emotional, and compulsive consumption

- Chapter 8 — Accumulated consequences: financial and emotional impacts in the long term

- Chapter 9 — Awareness without guilt: the boundary between understanding impulse and controlling it

- Frequently Asked Questions

- Recommended Reading

- Editorial Conclusion

- Research Context

- Editorial Disclaimer

- References

Chapter 1 — Why impulse spending begins with emotional triggers

Buying does not always begin with a conscious decision. In many contexts, it begins with a specific emotional state. Before reason organizes pros and cons, the body has already responded to the environment and the pressures of the day: mental exhaustion, accumulated tension, diffuse frustration, or silent anxiety. In this scenario, the act of consuming stops operating as a deliberate choice and begins to function as a response. It becomes a quick, accessible, and socially accepted reaction to momentary emotional discomfort.

Economic and behavioral psychology observe that financial decisions do not occur in a cognitive vacuum. They emerge from specific mental states, shaped by emotions, context, and the cognitive load available at the moment of choice. When this state is one of exhaustion or tension, consumption tends to assume a regulatory function, even if this is not consciously recognized.

Consumption as an immediate emotional trigger and regulator

Intense emotional states tend to seek rapid resolution. The literature on self-regulation shows that negative emotions temporarily reduce executive control capacity, shifting focus from the long term to immediate rewards (Baumeister, Vohs & Tice, 2007). In these moments, the brain begins to prioritize actions that promise quick relief, even if future costs are not fully considered.

Buying something small, available, and easily justifiable offers exactly this type of immediate reward. The central element is not the objective utility of the product, but the subjective feeling associated with acquiring it. Studies in neuroeconomics indicate that the anticipation of a purchase activates dopamine-related reward systems, producing a temporary sense of relief or pleasure even before possession of the good (Knutson et al., 2007).

In this sense, consumption functions as an improvised emotional regulator. It does not eliminate the source of discomfort, but it creates a subjective pause. During this interval, tension seems reduced, the sense of control momentarily returns, and the emotional state stabilizes for a few moments. The brain learns through association: purchasing becomes linked to the reduction of distress.

This learning occurs through repetition and does not require conscious intention. Over time, the purchase stops responding to a clear external need and begins responding to a recurring internal state. This dynamic helps explain why financially informed and aware individuals still make impulse purchases in specific contexts. The issue is not a lack of knowledge, but the emotional function that the act of consuming assumes at that moment.

This logic connects directly to broader discussions about why financial decisions often conflict with rational intentions, explored in Article #21, The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions.

From deliberation to reaction in the decision-making process

When consumption operates as an emotional response, the decision-making process shortens. Steps traditionally associated with financial decisions, such as identifying the need, evaluating alternatives, comparing prices, and considering budget impact, are compressed or ignored. The decision occurs before deliberation is complete.

Daniel Kahneman describes this phenomenon as the predominance of fast, intuitive thinking over slow, analytical thinking (Kahneman, 2011). Under stress or mental fatigue, the analytical system loses strength. The brain seeks cognitive shortcuts that reduce effort and discomfort. Consumption, especially when it involves relatively low amounts or simple justifications, fits perfectly into this pattern.

Rationalization appears afterward. The individual constructs plausible explanations for a decision that was already made emotionally: the price seemed low, the item was useful, the timing was favorable, or there was a sense of deservingness involved. These justifications are not necessarily false, but they were not the primary driver of the action. They function as a subsequent narrative, not as the cause.

Research on decision fatigue shows that throughout the day, the capacity to evaluate costs and benefits decreases significantly, while the propensity for automatic decisions increases (Vohs et al., 2008). In this state, consumption ceases to be evaluated as a financial choice and begins to be executed as a functional response to cognitive exhaustion.

Everyday contexts that transform emotions into consumption

An extreme event is not required to activate this mechanism. Small accumulated pressures create an emotional background favorable to reactive consumption. Successive deadlines, constant interruptions, minor conflicts, task overload, and a persistent sense of lack of time create a state of continuous wear. Consumption responds to this general state, not to an isolated stimulus.

Institutional reports on financial well-being observe that high levels of stress are associated with less planned financial decisions, even among individuals with stable income (Federal Reserve Board, 2026). This association does not indicate irresponsibility, but adaptation. In emotionally demanding environments, quick decisions tend to replace optimized decisions.

Research in the sociology of consumption also points out that the act of buying often functions as a mechanism of symbolic compensation in the face of feelings of loss of control or everyday frustration (Dittmar, 2008). The acquired object temporarily assumes the role of restoring emotional balance, even if in a limited and transient way.

This pattern is especially relevant for women, who often accumulate multiple layers of responsibility related to work, care, and everyday management. Studies on mental load indicate that overlapping roles reduce the cognitive space available for financial deliberation in moments of exhaustion (OECD, 2025). In these contexts, consumption may emerge as one of the few immediate responses available to accumulated emotional discomfort.

This relationship between overload, emotions, and financial decisions appears transversally in how women’s money stories shape emotional spending, explored in Article #74.

The social validation of purchasing as an emotional response

Another central element is the cultural normalization of consumption as a legitimate form of emotional response. Buying to relieve the day, reward effort, or restore morale is widely accepted and socially reinforced. Advertising, self-care discourse, and narratives of deservingness contribute to this framing.

Unlike other reactions to stress, consumption is socially validated. It is presented as a practical, harmless, and even desirable solution. This validation reduces moral friction at the moment of decision. If the response is perceived as legitimate, there is no incentive to interrupt or question it at that instant.

The conflict arises only later, when the emotional effect dissipates and the purchase must be integrated into the budget, physical space, or medium- and long-term financial goals. It is at this point that cognitive dissonance appears, described by Festinger, between momentary satisfaction and the subsequent consequences of the decision (Festinger, 1957).

Normalization also makes the pattern harder to identify. When consumption is framed as an isolated personal choice, it becomes more difficult to recognize it as an automatic response conditioned by context and internal state. This erasure of context favors narratives centered on self-control rather than structural analyses of consumption behavior.

Recognizing consumption as an emotional response

Understanding consumption as an emotional response shifts the analytical focus from the traditional question. Instead of questioning only the object purchased, it becomes necessary to observe the emotional state and context that preceded the decision. This shift is essential to avoid simplified explanations based exclusively on willpower or individual discipline.

By recognizing that many purchases arise as predictable responses to specific emotional states, space opens for a more precise analysis of the mechanisms that anticipate the decision. This chapter does not conclude the theme, but establishes the cognitive foundation of the article. From this framing, it becomes possible to examine how seemingly neutral stimuli activate purchase impulses before conscious reflection is triggered, preparing the transition to the analysis of invisible triggers developed in the next chapter.

Chapter 2 — Invisible triggers: how everyday stimuli anticipate the purchase decision

The decision to buy rarely originates at the moment the product is seen. In many cases, it has already been prepared beforehand by stimuli that operate below the level of deliberate consciousness. These invisible triggers do not persuade through rational arguments, nor do they depend on active reflection. They work by activating emotional associations, fast expectations, and learned responses, creating favorable conditions for the purchase to happen almost automatically. This chapter analyzes how everyday stimuli anticipate the consumption decision before conscious reflection is activated.

Sensory and emotional stimuli in the consumption environment

Consumption environments are organized to induce specific emotional states. Lighting, colors, sounds, spatial arrangement, and the pace of movement directly influence the consumer’s mood and level of attention. Environmental psychology shows that these stimuli change how people perceive comfort, safety, and pleasure, affecting the propensity to buy without this influence being consciously identified (Mehrabian & Russell, 1974).

These elements do not communicate objective information about utility or price. They modulate affective states. Welcoming environments tend to reduce cognitive vigilance. Stimulating environments raise emotional arousal. In both cases, the outcome is similar: less resistance to the impulse to consume. Classic studies on consumer behavior indicate that positive emotions increase impulse purchases, while negative emotions can direct consumption as an attempt at emotional relief (Rook, 1987).

The central point is that these stimuli do not need to be intense. Small sensory changes, when combined, create an emotional climate that prepares the individual to act, not to evaluate critically. When the product appears, it encounters a mental state already inclined toward action.

Cognitive triggers and automatic associations

Beyond sensory stimuli, cognitive triggers play a decisive role in anticipating the decision. Phrases such as “limited-time offer,” “only a few left,” or “special edition” activate mental heuristics associated with scarcity and urgency. These heuristics function as cognitive shortcuts that simplify complex decisions, especially under pressure or high mental load.

The literature on heuristics and biases shows that, in the face of uncertainty or time constraints, the brain replaces detailed analysis with fast rules based on previous experiences (Tversky & Kahneman, 1974). The perception of scarcity, for example, increases the item’s subjective value, regardless of its real utility. The trigger does not inform. It signals that the decision must be made quickly.

These associations become more automatic as they are repeated. Constant exposure to certain signals reinforces learned responses, reducing the space for conscious deliberation. The consumer tends to interpret this reaction as spontaneous, when in practice it was prepared by a predictable sequence of cognitive stimuli.

This dynamic connects with broader discussions about why financial decisions often drift away from rational intentions, as analyzed in Article #21.

Personalization, repetition, and the anticipation of choice

In digital environments, invisible triggers operate with greater precision. Recommendation algorithms use browsing history, past purchases, and behavioral patterns to present highly personalized stimuli. The effect is not limited to convenience. It is the anticipation of choice.

Research in behavioral economics indicates that familiarity reduces decision friction. When a stimulus matches preferences already demonstrated, the brain recognizes the pattern and responds more quickly, requiring less cognitive effort (Ariely, 2008). The decision feels natural because it fits within an already known repertoire. The impulse is reactivated, not created from scratch.

Constant repetition of these stimuli produces normalization. Seeing similar products, recurring messages, and personalized reminders reinforces the perception that the purchase is appropriate at that moment. The boundary between desire and action progressively shortens. This process helps explain why impulse spending intensifies in digital environments and connects to the normalization of credit and debt in everyday financial life, discussed in how everyday spending patterns affect household debt and stability.

Emotional states as amplifiers of triggers

Invisible triggers do not operate in isolation. They are amplified by specific emotional states. Stress, mental fatigue, and a sense of overload reduce the ability to filter stimuli and increase susceptibility to simple signals. In these states, triggers that might be ignored under calm conditions become decisive.

Studies on cognitive load show that, when the mind is occupied, individuals become more vulnerable to external influences and less able to resist immediate impulses (Shiv & Fedorikhin, 1999). The brain seeks to conserve mental energy, prioritizing automatic responses. The anticipation of the decision occurs because the effort to deliberate is perceived as an additional cost.

This effect is particularly relevant in everyday contexts of high emotional demand. For many women, the combination of professional responsibilities, caregiving, and household management creates an environment conducive to cognitive fatigue. Under these conditions, consumption triggers encounter less internal resistance. The impulse does not reflect individual fragility, but a specific mental state shaped by context.

This relationship between emotions, context, and financial decisions appears transversally in how women’s money stories shape emotional spending, which examines how emotional experiences shape spending patterns over time.

When the decision is prepared before it is perceived

The convergence of sensory stimuli, cognitive triggers, digital personalization, and emotional states results in a central phenomenon for this article. The purchase decision is often prepared before it is perceived as a decision. At the moment the consumer believes they are choosing, much of the process has already occurred automatically.

Research in consumer neuroscience indicates that fast emotional responses precede rational evaluations, especially in decisions with apparently low risk (Bechara & Damasio, 2005). Conscious awareness enters later to organize plausible explanations, not to command the act. This inversion helps explain why regret tends to arise after the purchase, not before it, a theme that will be explored in greater depth in the next chapters.

Recognizing this mechanism shifts the analytical focus. The question stops being why someone decided to buy and becomes how the decision was constructed over time. Invisible triggers do not eliminate individual agency, but they create structural conditions that make impulse more likely, reducing the space for conscious deliberation.

Chapter 3 — The role of stress, mental fatigue, and emotional overload

The influence of consumption triggers does not manifest uniformly. It depends on the mental state the individual is in at the moment of exposure. Stress, mental fatigue, and emotional overload do not create the impulse to buy by themselves, but they profoundly alter how stimuli are processed. This chapter analyzes how these states reduce the capacity for conscious deliberation and increase the effectiveness of the invisible triggers described earlier.

Stress as a reducer of evaluative capacity

Psychological stress changes cognitive functioning. Under stress, the organism prioritizes fast responses oriented toward the immediate resolution of discomfort. The psychology literature shows that high levels of stress are associated with reduced working memory and a diminished ability to evaluate future consequences, favoring short-term decisions (McEwen & Sapolsky, 1995).

In the context of consumption, this means that the assessment of price, utility, and financial impact loses centrality. The focus shifts to the possibility of immediate relief. Studies in behavioral economics indicate that individuals under stress tend to overvalue instant rewards and underestimate future costs, a phenomenon often associated with hyperbolic discounting (Haushofer & Fehr, 2014).

In these cases, consumption is not perceived as a strategic financial decision, but as a functional response to a state of tension. The purchase presents itself as a concrete action in an environment where other sources of control seem limited. This shift helps explain why impulse spending intensifies during periods of continuous pressure, even when there is no objective change in income or material needs.

This dynamic connects with broader analyses of how contexts of insecurity and pressure affect economic decisions, discussed in Why Financial Crises Always Come Back — Historical Patterns and Lessons for Women.

Mental fatigue and the depletion of self-regulation

Mental fatigue operates in a complementary way to stress. Throughout the day, successive decisions consume cognitive resources. As these resources are depleted, it becomes harder to sustain self-control and careful evaluation. Research on self-regulation shows that the ability to resist impulses decreases after prolonged periods of cognitive effort (Baumeister et al., 2007).

In this state, the brain tends to adopt energy-saving strategies. Automatic decisions replace deliberate decisions. Impulse spending emerges not because the individual wants to spend more, but because evaluating alternatives becomes cognitively costly. The purchase becomes a simple solution at a moment of mental exhaustion.

Experimental studies show that mentally fatigued people are more likely to accept default options, respond to salient stimuli, and avoid choices that require detailed comparison (Vohs et al., 2008). In consumption environments, this means greater susceptibility to highlighted offers, personalized suggestions, and urgency messages.

This relationship between mental fatigue and financial decisions also appears in analyses of why financial planning fails in everyday contexts, even among informed individuals, as discussed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions.

Emotional overload and the search for symbolic relief

Emotional overload differs from acute stress. It is characterized by the ongoing accumulation of unresolved emotional demands. Multiple responsibilities, conflicting expectations, and lack of time for emotional recovery create a persistent state of wear. In this context, consumption can take on a symbolic compensatory function.

Research in the sociology of consumption indicates that impulse purchases often function as an attempt to restore emotional balance or a threatened identity, even if only temporarily (Dittmar, 2008). The acquired object does not resolve the overload, but it offers a momentary sense of care, control, or reward.

This mechanism is particularly relevant for women, who tend to carry a greater emotional burden related to caregiving, household management, and mediating social relationships. OECD studies show that women perform more unpaid work and experience greater daily mental load, which contributes to higher levels of emotional exhaustion (OECD, 2025).

In this scenario, consumption does not appear as excess, but as adaptation. It fits into an emotionally demanding routine as one of the few available responses that does not require negotiation, justification, or postponement. This perspective helps explain why patterns of emotional spending persist even when they produce regret afterward.

The relationship between emotional overload, gender, and financial decisions is explored more broadly in Why Women’s Money Stories Shape Emotional Spending and Financial Independence.

Interaction between internal states and external stimuli

Stress, mental fatigue, and emotional overload do not act in isolation. They interact with the external stimuli described in the previous chapter, amplifying their effects. A trigger that could be ignored in a calm state becomes highly effective in a state of emotional exhaustion.

Studies in cognitive psychology show that emotional load reduces the ability to filter irrelevant stimuli, increasing the influence of salient signals in the environment (Shiv & Fedorikhin, 1999). This means that the anticipation of the purchase decision depends not only on the trigger, but on the mental state that receives it.

This interaction explains why the same individual can resist impulses at certain moments and give in at others, without this indicating inconsistency in values or goals. Behavior varies because deliberative capacity varies. Impulse spending, in this sense, is contingent, not random.

How mental states shape the space of choice

Recognizing the role of stress, mental fatigue, and emotional overload makes it possible to understand that the space of choice is not fixed. It expands or contracts according to the individual’s internal state. In moments of balance, there is room for reflection. In moments of depletion, that room shrinks drastically.

This chapter establishes that the decision to consume occurs not only as a function of external stimuli, but within a specific emotional field that determines how much deliberation is possible. By understanding how mental states shape this field, it becomes possible to move forward to the analysis of the next chapter, which will examine why the act of buying provides a feeling of immediate reward and psychological relief, even when its consequences are ambivalent.

Chapter 4 — Immediate reward and psychological relief in the act of buying

Impulse spending is sustained not only by the anticipation of the purchase or by reduced conscious deliberation. It consolidates because the act of buying produces a specific psychological experience, marked by a feeling of reward and immediate relief. This chapter examines why buying generates momentary well-being, how this effect is processed cognitively, and why it tends to disappear quickly, making room for later regret.

The reward circuit activated by buying

The experience of buying activates brain mechanisms associated with reward. Studies in neuroeconomics show that the anticipation of an acquisition activates areas linked to the dopaminergic system, responsible for feelings of pleasure and motivation (Knutson et al., 2007). This effect occurs even before possession of the product. The simple act of choosing and confirming the purchase already produces a positive emotional response.

This functioning helps explain why impulse is so difficult to interrupt at the moment it arises. The brain responds to consumption as if it were facing an opportunity for immediate emotional gain. The reward is not tied to the object’s future use, but to the acquisition process itself. Buying becomes an autonomous emotional experience.

The behavioral psychology literature observes that immediate rewards tend to be overvalued relative to future benefits, especially under stress or mental fatigue (Kahneman, 2011). In this context, the immediate pleasure of buying overrides the financial cost that will only be fully felt later. The decision is not irrational; it follows the logic of a cognitive system oriented toward the short term.

This dynamic connects with broader analyses of why financial decisions often conflict with long-term rational intentions, discussed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions.

Buying as a form of psychological relief

Beyond reward, the act of buying often produces relief. In states of stress or emotional overload, the purchase functions as a temporary interruption of discomfort. It offers a sense of resolution, even if symbolic. Something was done, a concrete action occurred, and that momentarily reduces internal tension.

Research in consumer psychology indicates that impulse purchases are often used as an emotional regulation strategy, especially to deal with negative emotions such as frustration, sadness, or a sense of loss of control (Rook & Gardner, 1993). Consumption does not eliminate the cause of distress, but it creates a subjective pause that is experienced as emotional improvement.

This relief is socially reinforced. Buying is a culturally accepted response to emotional depletion. Unlike other forms of regulation, such as avoiding tasks or externalizing conflicts, consumption is legitimized as self-care or deservingness. This validation reduces internal conflict at the moment of decision, making relief more accessible.

However, the symbolic nature of this relief is central. It does not result from resolving the original problem, but from the feeling of action and reward. For this reason, it tends to be brief. When the emotional state returns or when financial reality asserts itself, the effect dissipates.

The temporal asymmetry between pleasure and cost

One of the structural elements of impulse spending is the temporal asymmetry between pleasure and cost. Pleasure occurs in the present, while cost is postponed. This temporal separation favors decisions that maximize immediate well-being, even when they generate undesirable consequences in the future.

Behavioral economics describes this phenomenon as temporal discounting. Individuals tend to assign less weight to future costs than to immediate benefits, especially when those benefits involve positive emotions (Laibson, 1997). In impulse spending, this asymmetry is amplified by payment methods that reduce the perception of spending, such as credit cards or digital payments.

Institutional reports indicate that the dissociation between the act of buying and the perception of payment contributes to a greater propensity for unplanned spending (Federal Reserve Board, 2026). The financial cost becomes abstract at the moment of decision, while pleasure is concrete and immediate. This combination creates an environment favorable to repeating the behavior.

This logic connects with analyses of how credit card convenience makes spending feel less real, explored in Article #45.

Why the effect does not last

Despite the intensity of the initial reward, the emotional effect of buying tends to be transitory. Studies show that the satisfaction associated with material acquisitions declines quickly after the purchase, a phenomenon known as hedonic adaptation (Brickman & Campbell, 1971). The new object loses its capacity to generate pleasure as it becomes integrated into routine.

When the reward dissipates, the individual returns to the prior emotional state or faces new states of discomfort. At that point, the cost of the decision begins to become visible. The spending must be incorporated into the budget, physical space is taken up, and coherence with medium- and long-term financial goals is questioned. It is at this point that regret tends to arise.

The contrast between initial pleasure and later evaluation creates cognitive dissonance. A decision that made emotional sense at the time of purchase can appear inadequate under rational analysis. This mismatch does not invalidate the earlier emotional experience, but it highlights its temporal limitation.

This transition between reward and regret will be explored in greater depth in the next chapter, which examines why critical evaluation usually occurs afterward, not before, the purchase decision.

The role of repetition in consolidating the pattern

The combination of immediate reward and psychological relief creates a reinforcement cycle. Whenever a purchase produces relief, even briefly, the behavior is reinforced. The brain registers the association between consuming and feeling better, increasing the probability of repetition in similar contexts.

This cycle does not require total loss of control or lack of financial knowledge. It consolidates precisely because it operates at automatic levels, reinforced by everyday experiences. Over time, impulse spending can become a recurring response to certain emotional states, even when the individual recognizes its negative consequences.

Understanding this mechanism is essential to shift the analysis from moral judgment to structural understanding. Impulse spending persists not because people ignore its costs, but because immediate emotional reward precedes and overrides the evaluation of those costs at the moment of decision.

By establishing how reward and psychological relief sustain the impulse to buy, this chapter prepares the transition to the next analysis. The next step is to understand why, despite this initial relief, regret tends to emerge after the purchase, when the emotional effect has already dissipated and the decision must be reinterpreted rationally.

Chapter 5 — Digital environments, reduced friction, and the acceleration of impulse

Impulse spending gains intensity when it moves into digital environments. Not only because the offer is larger or more accessible, but because the architecture of these environments reduces frictions that, in the physical world, functioned as natural pauses for reflection. This chapter analyzes how digital platforms shorten the time between stimulus and action, accelerating the impulse to buy and pushing the decision even further outside the realm of conscious deliberation.

The reduction of friction as a structural principle

Friction, in the context of decision-making, refers to any element that introduces delay, effort, or cognitive cost before action. In physical environments, friction is implicitly present. One must travel, compare products, stand in lines, and make visible payments. Each of these steps creates small interruptions that can reactivate rational evaluation.

Digital environments are designed to eliminate these interruptions. Saved cards, one-click payments, automatic authentications, and purchase history reduce the number of intermediate decisions. Buying stops being a process and becomes a gesture. Research in behavioral economics shows that reducing friction significantly increases the likelihood of impulsive decisions, even when the monetary value remains the same (Sunstein, 2017).

The effect is not neutral. By removing intermediate steps, the digital environment reduces the temporal space needed for analytical thinking to be activated. The decision occurs in an interval so short that reflection becomes practically optional. Impulse finds a direct path to action.

Speed, convenience, and the compression of decision time

Acceleration is another central element. Digital platforms operate at a pace faster than the human capacity for deep evaluation. Notifications, time-limited offers, and constant updates create the feeling that the moment to decide is always now.

The literature on decision-making indicates that time pressure favors automatic choices and reduces the consideration of alternatives (Ariely, 2008). When the perceived time to decide is short, the brain relies on simple heuristics. Buying becomes more likely because it is the fastest option to end decisional tension.

This mechanism is reinforced by messages that associate speed with efficiency. Buying quickly is presented as an advantage, not a risk. Convenience comes to be interpreted as a gain, even when it implies loss of control over the decision-making process. This shift helps explain why many digital purchases are described as “they happened before I even realized.”

This logic connects with analyses of how everyday financial life is reorganized around convenience, discussed in Household Debt and Economic Stability: Why Growth Alone Tells the Wrong Story.

Algorithmic personalization and the anticipation of desire

Digital environments do not only reduce friction. They anticipate desires. Algorithms analyze browsing patterns, purchase history, time spent, and prior interactions to present stimuli highly tailored to the user’s profile. The psychological effect is not only relevance, but familiarity.

Research in cognitive psychology indicates that familiar stimuli require less processing effort and tend to be evaluated more positively (Zajonc, 1968). When the product presented seems to “match” past preferences, the decision occurs with less internal resistance. The impulse does not need to be built; it is reactivated.

This anticipation creates the feeling that the choice is spontaneous and personal, when, in practice, it was prepared by repetition and algorithmic learning. The line between one’s own desire and external suggestion becomes blurred. The consumer reacts to stimuli that seem to appear at exactly the right moment, reinforcing the perception of opportunity.

This dynamic connects to broader discussions about algorithmic mediation of financial decisions and how it influences spending patterns over time, a theme that appears transversally in Why Women’s Money Stories Shape Emotional Spending and Financial Independence.

Digital payments and the abstraction of cost

Another decisive factor is the payment method. In digital environments, the act of paying tends to be abstracted. There is no physical exchange of money, nor an immediate perception of loss. Payment occurs as an invisible step, often after the emotional decision has already been made.

Studies show that less salient payments reduce the “pain of paying” and increase the propensity to spend (Prelec & Loewenstein, 1998). Credit cards, digital wallets, and automatic payments separate the pleasure of the purchase from the financial cost in time. The brain registers the reward but postpones the sensation of loss.

Federal Reserve reports note that consumers who use digital payment methods report a lower perception of the immediate impact of spending, even when they review their statements afterward (Federal Reserve Board, 2026). This dissociation reinforces the impulsive pattern because cost does not function as a brake at the moment of decision.

This logic is deepened in analyses of how credit convenience changes the subjective experience of consumption, explored in The Hidden Cost of Credit Card Convenience.

Always-on environments and the absence of cognitive recovery

Digital environments are also characterized by constant availability. There is no closing time, pause, or clear temporal limitation. This continuity reduces opportunities for cognitive recovery. The individual remains exposed to consumption stimuli even during moments of rest, leisure, or emotional recovery.

Research on cognitive fatigue indicates that the absence of intervals increases vulnerability to automatic decisions (Vohs et al., 2008). When the mind does not recover, the capacity to resist impulses progressively diminishes. The digital environment, by remaining always active, amplifies this vulnerability.

For many women, who already operate under high daily mental load, this continuous exposure adds to other sources of depletion. Digital consumption enters moments of exhaustion, not planning. Impulse finds an even more favorable terrain.

How digital architecture redefines impulse

By combining reduced friction, acceleration, personalization, and cost abstraction, digital environments redefine the experience of impulse spending. The decision is not only emotional. It is structurally facilitated. Impulse travels a short, fast, and barely visible path to action.

This chapter establishes that the environment is not neutral. It shapes the space of choice and redefines what it means to decide. By understanding how digital architecture accelerates impulse, it becomes possible to move forward to the analysis of the next chapter, which will examine why, despite this apparent fluidity, regret tends to emerge after the purchase, when cost finally becomes concrete and rational evaluation returns.

Chapter 6 — Why regret emerges after, not before, the purchase

Regret associated with impulse spending rarely appears at the moment of decision. It emerges later, when the initial emotional experience has already dissipated and the purchase must be integrated into the individual’s financial and symbolic reality. This chapter analyzes why critical evaluation usually occurs after the fact, how emotions and cognition operate on different timelines, and how this mismatch structures the impulse spending cycle.

The temporal separation between emotion and evaluation

At the moment of purchase, the emotional system takes center stage. Intense affective states, environmental triggers, and reduced friction direct action toward the present. Rational evaluation, in turn, operates on a different timeline. It requires emotional distance, attention, and available cognitive resources.

Cognitive psychology describes this phenomenon as alternation between automatic processing and reflective processing. In situations of high emotional load or contextual pressure, automatic processing prevails. Reflective processing tends to be reactivated only when the stimulus disappears and the emotional state stabilizes (Kahneman, 2011). Regret emerges precisely at this moment of reactivation.

This explains why many people report that the purchase “made sense at the time.” It truly did, within the cognitive system that was active in that instant. The issue is not individual inconsistency, but a change in mental state. The decision was made in an emotional context that no longer exists when the later evaluation occurs.

This dynamic connects to broader analyses of why long-term financial intentions often conflict with everyday decisions, discussed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions.

The role of post-purchase rationalization

After the purchase, the individual tends to build explanations for the decision that was made. This rationalization process is not necessarily defensive. It functions as an attempt to maintain internal coherence between action and personal values. Cognitive dissonance theory suggests that, when there is conflict between behavior and beliefs, the brain seeks to reduce discomfort by adjusting internal narratives (Festinger, 1957).

In the short term, rationalization can soften regret. Justifications such as future usefulness, deservingness, or opportunity help sustain the decision. However, as time passes and costs become more visible, these narratives lose strength. The spending must be incorporated into the budget, the bill arrives, or the object loses emotional relevance.

When rationalization is no longer sufficient, regret emerges. It does not indicate that the decision was irrational at the moment it occurred, but that the context of evaluation has changed. The purchase begins to be analyzed under different criteria than those that generated it.

The delayed visibility of cost

Another central factor in delayed regret is the visibility of cost. In many impulse spending contexts, especially digital ones, the financial cost is abstract at the moment of decision. Automatic payments, credit, and installment plans dissociate the pleasure of the purchase from the financial impact over time.

Studies in behavioral economics show that the so-called “pain of paying” is reduced when payment is less salient or occurs at a different moment than the purchase (Prelec & Loewenstein, 1998). Cost, therefore, does not function as an immediate brake. It reappears later, when the statement is reviewed or when it limits future choices.

Federal Reserve reports indicate that consumers often underestimate the cumulative impact of small, recurring expenses, perceiving their effects only when the budget becomes tighter (Federal Reserve Board, 2026). In this case, regret is not tied to the isolated value of the purchase, but to the sum of decisions that begin to compete with other financial priorities.

This logic connects with analyses of how credit convenience changes cost perception and contributes to persistent patterns of financial regret, explored in The Hidden Cost of Credit Card Convenience.

Regret as a cognitive signal, not a moral failure

Regret is often interpreted as a sign of personal error or lack of control. However, from a cognitive perspective, it functions as an informational signal. It indicates that the decision was reevaluated under new criteria and in a new emotional state.

Decision psychology suggests that emotions such as regret play an adaptive role. They help individuals adjust future expectations and learn from past experiences (Zeelenberg & Pieters, 2007). The problem arises when regret is interpreted only as an individual failure, without consideration of the emotional and structural contexts that shaped the initial decision.

This moralizing interpretation tends to obscure the underlying pattern. Instead of understanding why the evaluation occurred too late, the focus shifts to self-censure. This shift makes it harder to identify recurring triggers and contributes to repeating the cycle.

This dynamic is particularly relevant for women, who often internalize a greater emotional burden for financial decisions, even when operating in structurally unfavorable contexts. The relationship between financial guilt, emotion, and consumption behavior is explored more broadly in Debt Is Not a Lack of Shame: The Emotional Healing of Financial Recovery.

The cycle of decision, relief, and regret

By bringing together the elements discussed, it becomes possible to outline a recurring cycle. First, a specific emotional state activates impulse. Next, the purchase provides immediate reward and relief. Then, with the return of reflective processing and the visibility of cost, regret emerges.

This cycle is not easily broken because each stage occurs on a different cognitive timeline. Learning is not automatic. Rationally recognizing that a purchase produced regret does not prevent the impulse from returning in another similar emotional context. The memory of regret competes with the memory of relief.

Understanding this cycle shifts the analysis from a single event to the observation of patterns. Regret is not the opposite of impulse, but part of the same process, emerging when the decision can no longer be reversed.

When evaluation returns to the center of the decision

This chapter establishes that regret emerges after the purchase because critical evaluation returns only when the emotional state and context change. The decision did not fail. It operated within a cognitive system oriented toward the present. Regret appears when another system takes control.

By recognizing this alternation, it becomes possible to move forward to the analysis of the next chapter, which examines the differences between impulsive, emotional, and compulsive consumption. This distinction is essential to avoid generalizations and to understand when impulse is episodic, when it becomes a pattern, and when it signals deeper processes of loss of control.

Chapter 7 — The difference between impulsive, emotional, and compulsive consumption

Not all unplanned spending is the same. Impulsive consumption, emotional consumption, and compulsive consumption are often treated as variations of the same behavior, but they operate through distinct mechanisms, have different psychological functions, and imply unequal consequences over time. This chapter establishes these distinctions to avoid generalizations and enable a more precise reading of spending patterns associated with emotions.

Impulsive consumption as a situational response

Impulsive consumption is, above all, situational. It occurs when a specific stimulus meets a favorable mental state, such as fatigue, stress, or momentary excitement. The decision is fast, minimally deliberated, and generally tied to a specific context. There is not necessarily prior intention to buy, nor systematic repetition of the behavior.

The classic literature on consumer behavior describes impulsive consumption as an immediate reaction to stimuli perceived as attractive or opportune, without prior planning and with a focus on the present (Rook, 1987). The central element is the absence of anticipation. The purchase happens because the context made it likely at that moment.

This type of consumption can produce later regret, but it does not imply ongoing loss of control. In many cases, it remains episodic. The individual recognizes the purchase as an exception, not as a pattern. For this reason, impulsive consumption, by itself, does not indicate financial or emotional dysfunction, although it can become problematic if frequent and cumulative.

This reading helps explain why people with organized financial habits still make impulsive purchases in specific situations, as discussed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions.

Emotional consumption as a recurring regulation strategy

Emotional consumption differs from impulsive consumption in the function it serves. It does not depend only on external stimuli, but responds to recurring emotional states. Buying, in this case, becomes a familiar strategy to deal with negative emotions or to amplify positive emotions. There is a more stable relationship between emotional state and consumption behavior.

Research in consumer psychology indicates that individuals turn to emotional consumption to regulate feelings such as sadness, frustration, loneliness, or overload, using the purchase as a coping mechanism (Dittmar, 2008). The decision may even involve some degree of anticipation, even if not fully conscious. The individual “knows” that buying will bring relief, even if temporarily.

Unlike impulsive consumption, emotional consumption tends to repeat in similar contexts. It is anchored in emotional patterns, not only in environmental stimuli. Regret may occur, but it coexists with the expectation of future relief. The purchase comes to be perceived as an available emotional resource.

This pattern is particularly relevant in contexts of chronic overload, in which other forms of emotional regulation are less accessible. The relationship between emotional histories, identity, and financial decisions is explored in Why Women’s Money Stories Shape Emotional Spending and Financial Independence.

Compulsive consumption as persistent loss of control

Compulsive consumption is qualitatively distinct from the other two. It involves persistent repetition of the behavior, a sense of loss of control, and significant difficulty interrupting the cycle even in the face of negative financial, emotional, or social consequences.

Clinical studies describe compulsive buying as behavior characterized by recurrent and intrusive urges to buy, followed by intense feelings of guilt, shame, or anxiety (Black, 2007). Unlike impulsive or emotional consumption, compulsive consumption does not depend only on context or a specific emotional state. It persists as a relatively autonomous pattern.

In this case, the purchase does not aim only at momentary emotional relief. It begins to function as an attempt to silence deeper discomforts, often associated with self-esteem, identity, or impaired emotional regulation. Relief is brief and is quickly replaced by additional distress, which reinforces the cycle.

It is important to emphasize that compulsive consumption cannot be understood only as an inappropriate financial choice. It belongs in the domain of mental health and requires a specific approach. Confusing compulsive consumption with ordinary impulsivity can lead to minimizing a problem that requires specialized attention.

Continuity and boundaries between patterns

Although distinct, these patterns are not airtight compartments. They are distributed along a continuum. Frequent impulsive consumption, when repeatedly associated with similar emotional states, can evolve into emotional consumption. Likewise, chronic emotional consumption can, in certain contexts, approach compulsive patterns.

The central difference is not the object purchased, but the psychological function of the purchase and the capacity to interrupt the behavior. The greater the difficulty of interrupting it, the greater the likelihood that the pattern approaches compulsion. The more dependent it is on specific emotional contexts, the more the behavior moves away from episodic impulsivity.

This distinction is fundamental to avoid excessive diagnoses or, conversely, the normalization of harmful patterns. Not all regret indicates compulsion. Not all impulsive purchases are emotional. A fine-grained understanding of these boundaries enables a more precise and less moralizing analysis.

Distinct financial and emotional implications

The consequences of these patterns also differ. Impulsive consumption tends to generate punctual and reversible financial impact. Emotional consumption can produce cumulative effects, especially when associated with credit or recurring spending. Compulsive consumption, in turn, often results in significant indebtedness, intense emotional suffering, and deterioration of one’s relationship with money.

Reports on financial well-being indicate that persistent patterns of emotional spending are associated with greater financial instability over time, even when income remains constant (Federal Reserve Board, 2026). In the case of compulsive consumption, impacts extend beyond the financial sphere and affect personal relationships and mental health.

Recognizing these differences helps reposition the analysis of consumption behavior. Instead of seeking a single explanation, it becomes possible to identify which pattern is operating in each situation.

Differentiating to understand, not to label

This chapter establishes that distinguishing between impulsive, emotional, and compulsive consumption is not intended to label behaviors, but to understand functions and limits. Each pattern responds to different contexts and requires different readings. Treating them all as a failure of self-control obscures underlying mechanisms and hinders appropriate interventions.

By clarifying these differences, the article moves on to the next chapter, which examines the accumulated consequences of these behaviors over time. From there, it becomes possible to analyze how seemingly small decisions add up and affect financial and emotional life more broadly, especially when these patterns remain invisible for long periods.

Chapter 8 — Accumulated consequences: financial and emotional impacts in the long term

Impulse spending rarely produces immediately evident harm. Its most significant effect emerges over time, when isolated decisions accumulate and begin to interfere with financial stability, the emotional relationship with money, and the perception of economic autonomy. This chapter analyzes how consumption behaviors that appear punctual become structural impacts in the long term, especially when they remain invisible or normalized.

The cumulative effect of small decisions

Much of the financial impact of impulse spending does not come from exceptionally high purchases, but from the repetition of moderate spending over time. Behavioral economics shows that individuals tend to underestimate the cumulative effect of small and frequent decisions, attributing little relevance to them at the moment they occur (Thaler, 1999).

Each isolated purchase seems manageable. The problem arises when these decisions begin to compete with medium- and long-term financial goals, such as saving, reducing debt, or building financial security. The budget does not collapse all at once. It narrows gradually. The space of choice shrinks without there being a single event that explains the loss of margin.

Reports on financial well-being indicate that many families report growing difficulty handling unexpected expenses even without significant changes in income, suggesting that erosion occurs silently and cumulatively (Federal Reserve Board, 2026). Impulse spending contributes to this erosion by reducing reserves and increasing vulnerabilities.

This dynamic connects with analyses of how everyday decisions shape household economic stability, discussed in Article #46.

The normalization of financial restriction

As accumulated effects manifest, a process of normalizing constraint occurs. Adjustments begin to be made repeatedly. Spending is reallocated, goals are postponed, and future choices become more limited. This process is rarely directly associated with past impulse spending. It is perceived as a generic result of the cost of living or external circumstances.

Research on mental accounting and behavioral decision-making suggests that people often separate small purchases into narrow categories instead of seeing their cumulative effect across the full budget (Thaler, 1999). This makes it harder to identify how repeated spending patterns contribute to financial restriction over time.

When restriction becomes part of everyday life, impulse spending can, paradoxically, intensify. The feeling of emotional or financial scarcity increases the search for immediate relief, reinforcing the cycle described in earlier chapters. The accumulated impact, therefore, is not only financial. It changes the emotional dynamics of one’s relationship with money.

Long-term emotional effects

Beyond financial consequences, recurring impulse spending produces lasting emotional effects. Repeated regret, even when mild, contributes to feelings of guilt, frustration, and loss of confidence in one’s decision-making capacity. Over time, these feelings shape the individual’s financial identity.

Research on regret regulation shows that repeated regret can influence future choices, avoidance, and emotional responses to decision-making (Zeelenberg & Pieters, 2007). Money stops being perceived only as a tool and can become a source of recurring emotional tension.

This effect is particularly relevant for women, who often internalize greater emotional responsibility for financial decisions, even when operating in contexts of structural overload. The combination of cumulative financial impact and self-blame contributes to an ambivalent relationship with consumption and financial planning.

This long-term emotional dimension appears repeatedly in analyses such as Debt Is Not a Lack of Shame: The Emotional Healing of Financial Recovery, which explores how guilt and shame shape financial trajectories.

The relationship between impulse spending and gradual indebtedness

Recurring impulse spending often connects to the gradual use of credit. Small installment plans, revolving limits, and deferred payments function as temporary buffers, allowing the spending pattern to continue without an immediately perceptible impact. Over time, these mechanisms turn isolated decisions into structural indebtedness.

Institutional data show that consumer indebtedness tends to grow incrementally, not abruptly, driven by recurring and unplanned expenses (Federal Reserve Board, 2026). Impulse spending acts as one of the vectors of this silent growth, especially when combined with the convenience of digital credit.

This logic connects with analyses of how credit changes the perception of cost and favors the persistence of patterns of emotional spending, discussed in The Hidden Cost of Credit Card Convenience.

Impacts on autonomy and future planning

As accumulated effects consolidate, financial autonomy is progressively reduced. Less budget margin means less ability to absorb shocks, take advantage of opportunities, or make choices aligned with long-term goals. Impulse spending, in this sense, does not affect only the present. It redefines the future that is available.

Research on temporal discounting shows that when immediate pressure dominates attention, future-oriented decisions tend to lose psychological weight (Laibson, 1997). When the relationship with money is marked by recurring regret, the time horizon tends to shorten.

This shortening of the horizon reinforces the cycle. The less the future is perceived as accessible, the greater the tendency toward decisions oriented to the present. Impulse spending stops being merely episodic behavior and begins to influence the architecture of future choices.

Consequences that become visible only with time

The main analytical challenge of impulse spending is the fact that its consequences are rarely immediate. They accumulate diffusely, diluted in everyday decisions and successive adjustments. When they become visible, the link to past decisions is no longer evident.

This chapter establishes that the impact of impulse spending must be evaluated over time, not in the isolated event. The behavior does not need to be extreme to produce structural effects. Silent repetition is enough.

By understanding these accumulated consequences, the article moves toward the final chapter of analytical development, which will examine how to recognize these patterns without resorting to guilt and where the boundaries lie between understanding, responsibility, and conscious control over consumption.

Chapter 9 — Awareness without guilt: the boundary between understanding impulse and controlling it

Understanding impulse spending does not mean eliminating it completely. It means recognizing its mechanisms, limits, and effects without turning that understanding into moral judgment. This final chapter articulates a point of balance: between awareness of the processes that precede a purchase and a realistic expectation of control that is possible within specific emotional and structural contexts.

Awareness as an expansion of the space of choice

Awareness does not act as an immediate brake on impulse. It expands the space of choice by making visible patterns that previously operated automatically. By recognizing that consumption decisions are influenced by emotional states, environments, and predictable triggers, the individual begins to interpret impulse in a contextualized way, not as an isolated failure.

Decision psychology indicates that awareness of heuristics and automatic responses does not eliminate them, but it can make recurring patterns easier to recognize over time (Tversky & Kahneman, 1974). Awareness does not stop impulse at the moment it arises, but it changes the internal environment in which future decisions will occur.

This shift is subtle. It does not operate in the register of rigid control, but in that of a more precise reading of one’s own behavior. The purchase stops being interpreted only as an individual act and begins to be understood as the result of specific conditions. This change reduces the negative emotional load associated with regret and creates space for a calmer evaluation.

The real limits of self-control

One of the most persistent misunderstandings in narratives about consumption is the overvaluation of self-control. The behavioral psychology literature shows that self-control is a limited resource and is highly context-dependent (Baumeister et al., 2007). Demanding constant control ignores the variability of emotional states and cognitive conditions throughout the day.

Recognizing limits does not mean abandoning responsibility. It means abandoning unrealistic expectations. Impulse cannot be managed in the same way in states of balance and in states of emotional exhaustion. Expecting identical performance in different contexts produces frustration and reinforces narratives of personal failure.

Awareness, in this sense, acts as a recalibration of expectations. It makes it possible to distinguish between decisions that could have been different and decisions that occurred within narrow cognitive margins. This distinction is essential to avoid cycles of self-blame that, paradoxically, increase the likelihood of new episodes of emotional consumption.

Responsibility without moralizing

Financial responsibility is often confused with constant vigilance and internal punishment. However, the analysis developed throughout this article suggests another reading. Responsibility involves recognizing recurring patterns and their effects, not denying the existence of impulses or demanding absolute control.

Moralizing consumption tends to obscure structural mechanisms. When attention focuses only on guilt, the opportunity to understand why certain contexts produce predictable responses is lost. Regret can support learning when it is treated as information, but it becomes less useful when it turns into self-condemnation (Zeelenberg & Pieters, 2007).

By replacing moralization with analytical observation, the individual preserves interpretive autonomy. Consumption stops being a field of judgment and becomes a field of understanding. This change does not eliminate regret, but it repositions it as an informative signal, not as personal condemnation.

This approach connects with broader reflections on financial recovery and emotional health, explored in Debt Is Not a Lack of Shame: The Emotional Healing of Financial Recovery.

Understanding impulse is not neutralizing it

There is a clear limit between understanding impulse and controlling it completely. Understanding does not guarantee immediate neutralization. It changes probabilities over time. Impulse spending may continue to occur, but it tends to lose the characteristic of absolute surprise.

Awareness creates small cracks in automaticity. In some moments, these cracks are enough to delay action. In others, they are not. The central point is that behavior begins to be interpreted within a broader frame in which context, emotion, and structure are considered together.

This reading prevents expectations of abrupt transformation. Changes in patterns of emotional consumption occur gradually and irregularly. They depend not only on intention, but on changes in the emotional environment and daily cognitive load.

Interpretive autonomy and one’s relationship with money

Over time, understanding one’s own consumption patterns influences the overall relationship with money. When decisions stop being interpreted as moral failures, the relationship tends to become less reactive and more reflective. Money stops being only a source of tension and becomes an object of ongoing analysis.

Research on financial well-being highlights the importance of savings, credit access, and perceived financial resilience in shaping household stability (Federal Reserve Board, 2026). This autonomy does not come from perfect control, but from a consistent understanding of one’s own limits and patterns.

In the context of women’s lives, this interpretive autonomy is particularly relevant. It makes it possible to shift individual narratives of guilt toward structural analyses, recognizing overload, pressures, and social expectations that shape consumption decisions unevenly.

Between understanding and possible control

This final chapter establishes that awareness of impulse spending operates in an intermediate space. It does not eliminate impulse, but it redefines how it is interpreted. Between understanding and controlling there is a field of continuous negotiation, in which decisions are influenced by emotional states, contexts, and structures that cannot be fully neutralized.

Recognizing this field does not weaken responsibility. On the contrary, it makes it more realistic and sustainable. Impulse spending stops being treated as an isolated deviation and begins to be understood as part of a system of imperfect yet understandable human decisions.

By closing this analytical path, the article returns interpretive autonomy to the reader over her own decisions. Understanding impulse does not mean eliminating it, but recognizing the contexts in which it arises, the limits of possible control, and the real space where financial choices are made.

Frequently Asked Questions

What is impulse spending?

Impulse spending is an unplanned purchase made with little time for reflection. It often happens when emotional pressure, urgency cues, digital convenience, or reduced payment friction make buying feel easier than pausing. The purchase may seem small or justified in the moment, but regret can appear later when the cost becomes clearer.

Why do I impulse buy even when I know I should save money?

Impulse buying can happen even when someone understands their financial goals. Stress, mental fatigue, emotional overload, and personalized shopping triggers can reduce the space for conscious decision-making. In that moment, buying may feel like relief, reward, or control, while the longer-term savings goal feels distant.

What are the most common impulse spending triggers?

Common impulse spending triggers include stress, boredom, fatigue, emotional discomfort, limited-time offers, personalized ads, one-click checkout, saved payment methods, social comparison, discounts, and the feeling of deserving a reward. These triggers become stronger when the buyer is tired, overwhelmed, or exposed to frictionless digital shopping environments.

Is impulse spending the same as emotional spending?

Impulse spending and emotional spending can overlap, but they are not exactly the same. Emotional spending is driven mainly by feelings, such as stress, sadness, frustration, or the desire for comfort. Impulse spending focuses on the speed and lack of reflection behind the purchase. A purchase can be impulsive, emotional, both, or neither.

Why does regret usually appear after an impulse purchase?

Regret often appears after an impulse purchase because the emotional state has changed. During the purchase, the buyer may feel relief, excitement, urgency, or justification. Later, when that feeling fades, the cost becomes more visible through a credit card balance, a tighter budget, or the realization that the item was not truly needed.

How do digital shopping platforms increase impulse spending?

Digital shopping platforms increase impulse spending by removing natural pauses from the buying process. Saved cards, one-click checkout, personalized recommendations, notifications, limited-time prompts, and digital wallets shorten the distance between desire and action. The easier it is to buy, the less time there is for reflection.

Can small impulse purchases really affect financial stability?

Yes. A single small purchase may not cause serious harm, but repeated impulse spending can quietly reduce savings, increase credit card balances, weaken budgeting confidence, and limit future choices. The long-term impact usually comes from accumulation, not from one isolated purchase.

When should impulse spending become a concern?

Impulse spending may become a concern when it repeatedly creates financial stress, debt, secrecy, emotional distress, or a feeling of being unable to pause before buying. Occasional unplanned purchases are common, but recurring patterns that harm well-being or financial stability may require deeper support, reflection, or professional guidance.

Editorial Conclusion

Impulse spending is often treated as a personal failure, but the psychology behind it is more complex. As this article has shown, buying on impulse usually emerges from the interaction between emotional pressure, stress, mental fatigue, digital design, urgency cues, payment convenience, and real cognitive limits. The purchase may feel spontaneous, but many triggers are already shaping the decision before conscious reflection has time to intervene.

This is why impulse spending should not be reduced to weak self-control. Invisible triggers prepare the moment, emotional overload makes the purchase feel more urgent or comforting, and low-friction digital environments shorten the distance between desire and action. For a few minutes, buying can feel like relief, reward, or control. The regret usually appears later, when the emotional charge fades and the financial cost becomes more visible.

Understanding this timing is central to the article’s argument. Regret does not necessarily mean the original decision made no emotional sense. It often means the decision is being reviewed from a different mental state, after the reward has passed and the budget impact, credit card balance, or lost financial margin becomes clearer. In that sense, regret can become a signal, not a reason for shame.

The distinction between impulse spending, emotional spending, and compulsive consumption also matters. Not every unplanned purchase is a serious problem, and not every emotional purchase reflects a loss of control. Some impulse spending is occasional. Some becomes a repeated way to regulate stress or exhaustion. And in some cases, patterns may become distressing enough to require specialized support. Clear distinctions make the conversation more honest, useful, and less moralizing.

The long-term impact of impulse spending usually appears through accumulation. One small purchase may not change a financial life, but repeated purchases made under emotional pressure can quietly reduce savings, increase credit card balances, weaken financial confidence, and make future choices feel more limited. The issue is not only the amount spent, but the pattern that forms when emotional triggers and frictionless systems repeatedly push decisions toward the immediate present.

For HerMoneyPath, the goal is not to tell women to become perfect decision-makers. Financial autonomy does not come from never feeling desire, stress, fatigue, or regret. It comes from recognizing patterns with clarity, understanding the environments that shape spending, and creating more space between the trigger and the purchase. When impulse spending is understood without guilt, it becomes easier to see where choice can be restored.

Research Context

This article draws on research from behavioral economics, consumer psychology, cognitive psychology, neuroeconomics, and financial well-being studies to explain why impulse spending often happens before a buyer fully recognizes the decision. The focus is not on blaming individuals for unplanned purchases, but on understanding how emotional states, environmental cues, digital design, and payment systems shape financial behavior.

Research on decision-making shows that people do not always evaluate purchases through slow, rational analysis. Under stress, fatigue, time pressure, or emotional overload, the mind often relies on faster and more automatic responses. In those moments, spending can feel like an immediate solution, especially when buying promises relief, reward, comfort, or a temporary sense of control.

Consumer psychology also shows that impulse buying is strongly influenced by external triggers. Urgency messages, discounts, personalized recommendations, social comparison, sensory cues, and repeated exposure can all make a purchase feel more attractive or harder to pause. In digital environments, these triggers become even more powerful because the distance between desire and action is shortened by saved cards, one-click checkout, digital wallets, and frictionless payment systems.

Studies in neuroeconomics and behavioral finance further suggest that the anticipation of buying can activate reward-related responses before the buyer has fully considered the cost. This helps explain why impulse spending can feel emotionally satisfying in the moment, even when the same purchase later produces regret. The pleasure of acquisition often arrives immediately, while the financial consequences become visible only afterward.

The research context also supports an important distinction between impulse spending, emotional spending, and compulsive consumption. These behaviors can overlap, but they are not the same. Impulse spending is defined by speed and reduced reflection. Emotional spending is driven primarily by feelings. Compulsive consumption involves more persistent and distressing patterns that may require specialized support. Treating all three as the same would oversimplify the psychology of money and weaken the usefulness of the analysis.

Within the HerMoneyPath editorial framework, this article uses research as a foundation for a practical and non-moralizing interpretation of everyday spending. The goal is to help readers understand how impulse spending begins, why regret often appears later, and how repeated small decisions can affect savings, credit card balances, financial confidence, and long-term autonomy over time.

Editorial Disclaimer