Money and Emotions: The Psychology of Why Spending Feels Good — and Why Regret Follows

Editorial Introduction

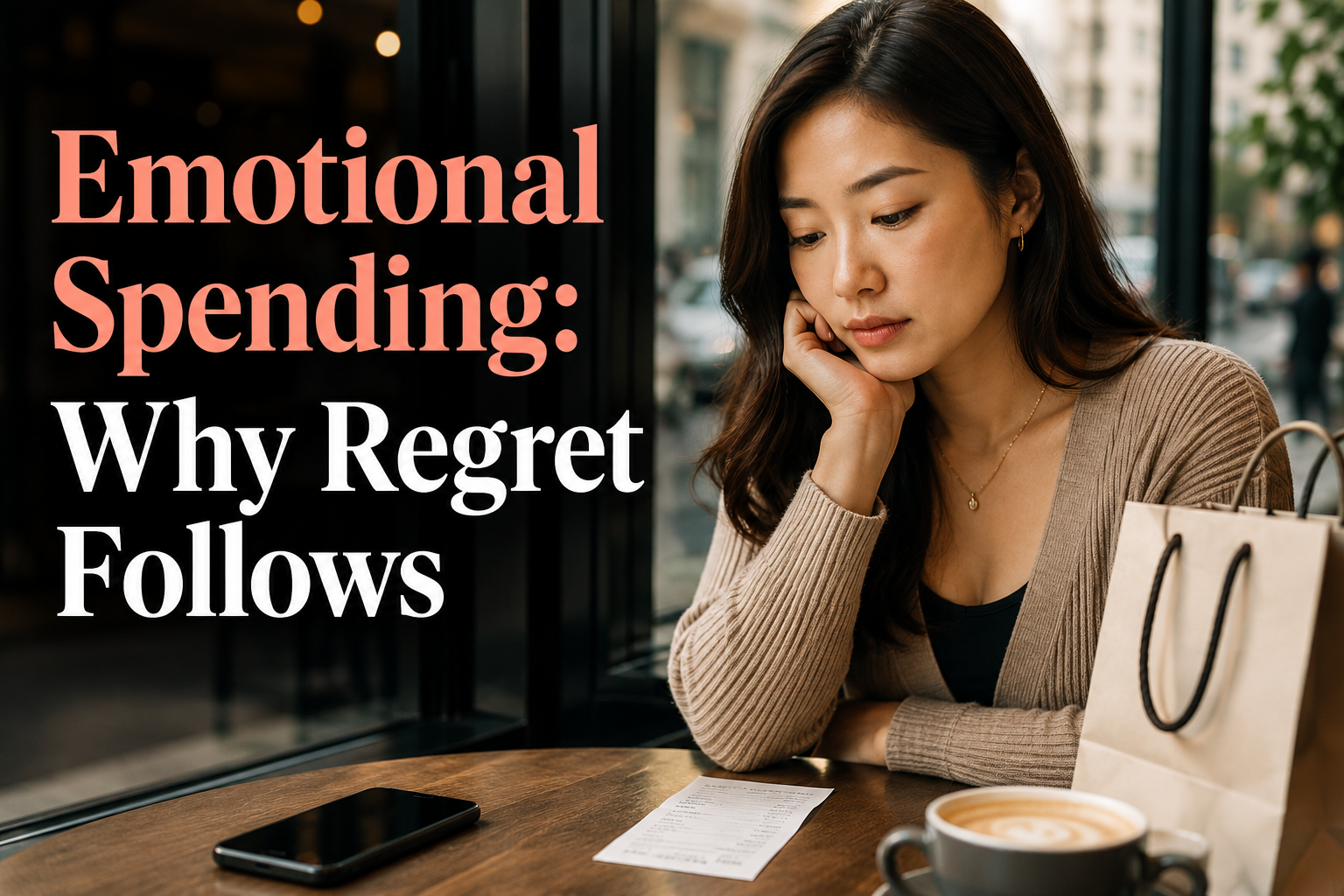

Emotional spending rarely begins with a dramatic financial decision. More often, it starts with a small moment of pressure: a stressful day, a feeling of exhaustion, a quick purchase that seems harmless, or the quiet desire to feel better for a few minutes. In that moment, buying can feel comforting, rewarding, and even reasonable.

But later, when the emotional intensity fades, the same purchase may look different. The pleasure that felt clear in the moment can turn into financial regret, guilt, or the uneasy question of why spending felt good at first but uncomfortable afterward. This article examines that emotional shift not as a failure of discipline, but as a psychological pattern shaped by stress, reward systems, digital environments, social expectations, and the meaning money carries in everyday life.

Throughout the article, emotional spending is analyzed as a sequence rather than a single mistake. The purchase may first appear as relief, reward, self-comfort, or a temporary sense of control. Regret often appears later, when the same decision is reinterpreted through bills, goals, debt, personal expectations, or the pressure to be financially responsible.

This distinction matters because financial decisions do not happen in isolation. Consumption environments, market language, personalized offers, and fast digital checkout systems can reduce friction and intensify emotional responses. At the same time, social and gender expectations can shape how spending is experienced and judged, especially for women, who are often expected to balance care, responsibility, restraint, and self-sacrifice around money.

Within the HerMoneyPath editorial system, this article is not a generic guide about spending less. Its purpose is to explain emotional spending psychology as the hidden passage from relief to regret: why buying can feel good in one moment and uncomfortable later. By understanding pleasure and regret as parts of the same human financial dynamic, the article invites a less punitive and more contextualized way to interpret everyday money decisions.

Quick Answer

Emotional spending feels good because buying can create quick relief, reward anticipation, and a temporary sense of control. Regret often follows when the emotional intensity fades and the purchase is judged against longer-term goals, bills, debt, or personal expectations. The pattern is not simply a lack of discipline; it reflects how stress, reward systems, digital environments, and money emotions interact.

Key Insights

- Emotional spending often begins before the purchase itself, when anticipation, stress relief, or the desire for comfort makes buying feel emotionally rewarding.

- The pleasure of spending is usually brief because it responds to an immediate emotional state, while regret often appears later when bills, goals, debt, or personal expectations return to focus.

- Financial regret is not simply proof of bad discipline; it can signal a conflict between short-term emotional relief and longer-term financial priorities.

- Digital shopping environments can intensify emotional spending by reducing friction, accelerating decisions, and making purchases feel easier in moments of stress or fatigue.

- For many women, spending decisions may carry added emotional weight because money is often tied to responsibility, care, self-worth, household expectations, and social judgment.

Chapter 1 — How Emotional Spending Psychology Begins in Everyday Financial Decisions

Emotions as the starting point of decision-making

Financial decisions rarely begin with conscious calculations or long-term projections. In most everyday situations, they emerge from emotional states that shape how options are perceived and evaluated at the moment of choice. Economic psychology observes that emotions function as initial cognitive filters, directing attention, urgency, and meaning before any deliberative reasoning is mobilized. This process does not represent an occasional failure of rationality, but a structural feature of human mental functioning.

Foundational research in behavioral economics demonstrates that individuals evaluate gains and losses in a relative manner, sensitive to context and present emotional state. The perception of value is neither fixed nor purely objective, being influenced by expectations, recent experiences, and momentary emotions (Kahneman & Tversky, 1979). In this sense, the act of spending cannot be understood solely as a response to prices or budget constraints, but as part of a broader psychological system of evaluation and internal regulation.

This is why emotional spending should not be reduced to a simple lack of discipline. In this article, the central issue is the emotional sequence behind the decision: stress or pressure creates the desire for relief, the purchase feels meaningful in the moment, and regret may appear later when the same decision is viewed through bills, goals, debt, or personal expectations.

Money as an emotional object

Money occupies a singular position in social life because it connects simultaneously to material and symbolic dimensions. It represents security, autonomy, belonging, and social recognition. These associations cause financial decisions to carry an emotional charge that extends beyond the monetary value involved. Even choices with low financial impact can activate intense feelings when associated with identity, status, or emotional relief.

Reports on financial well-being indicate that feelings of anxiety, insecurity, and stress are strongly correlated with how individuals perceive their economic situation, regardless of objective income or assets. The Report on the Economic Well-Being of U.S. Households observes that people with similar financial conditions may report very different levels of satisfaction or concern, suggesting that financial experience is mediated by emotional and subjective factors (Federal Reserve Board, 2023). This reinforces the idea that everyday economic behavior cannot be explained solely by objective indicators.

The influence of immediate emotional states

Transient emotional states exert direct influence on decision-making. Fatigue, frustration, boredom, or stress reduce cognitive availability for more complex analysis, favoring quick and intuitive choices. The psychology of self-regulation describes this phenomenon as a temporary reorganization of mental priorities, in which the individual seeks to restore emotional balance in the short term.

The strength model of self-control suggests that decisions under emotional load tend to prioritize immediate rewards, not due to lack of knowledge, but because of a momentary limitation of cognitive resources (Baumeister, Vohs, & Tice, 2007). In the financial context, this helps explain why individuals may act in ways that appear inconsistent with their own stated goals. Emotion does not eliminate rationality, but shifts its relative weight at the moment of choice.

Emotions as a structural component of economic behavior

The traditional view that opposes emotion and reason tends to treat feelings as undesirable noise in the decision-making process. However, accumulated evidence in psychology, neuroscience, and behavioral economics indicates that emotion and cognition operate in an integrated manner. There is no economic decision completely devoid of emotional content. Even choices considered prudent are sustained by emotions such as confidence, security, or loss aversion.

This integration challenges the moralizing narrative that associates emotionally motivated spending with individual failures of discipline. On the contrary, it suggests that financial behavior reflects adaptive mechanisms developed to cope with uncertainty and complexity. Spending may function as a legitimate response to internal states, even if it produces undesirable consequences when repeated systematically.

This approach dialogues with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by reinforcing that financial decisions are inseparable from the emotional contexts in which they occur. It also prepares the reader for the specific triggers behind impulse spending, where emotional buying is analyzed through the moments that anticipate the purchase decision.

Everyday life as a recurring decision space

A large portion of financial choices takes place in environments of low reflection and high repetition. Routine purchases, digital payments, and household decisions are made under multiple simultaneous demands, often without time or energy for in-depth evaluation. In these contexts, mild yet persistent emotions exert significant influence.

Behavioral economics describes this scenario as decision-making under cognitive load, in which available mental effort is limited. The result is the prevalence of simple heuristics and rapid emotional responses. The pleasure associated with small unplanned purchases, for example, is not an accident, but a direct consequence of this decision environment. It offers an immediate sense of control or reward amid exhausting routines.

Analytical implications of the emotional lens

Recognizing the role of emotions in financial decision-making does not imply denying individual agency or responsibility. On the contrary, it allows choices to be situated within concrete human limits. Instead of assuming fully rational agents, this analytical lens considers individuals embedded in specific emotional, social, and institutional contexts.

Studies in neuroeconomics indicate that brain areas associated with reward and emotion are activated simultaneously during financial decisions, including low-value choices. This overlap suggests that the economic decision system is deeply intertwined with basic emotional mechanisms responsible for guiding adaptive behavior throughout life.

Within the HerMoneyPath editorial system, this article occupies a specific role: it does not treat emotional spending as a budgeting mistake or a lack of discipline, but as a time-based emotional sequence. The central question is not only why someone spends, but why the same purchase can feel comforting in one moment and regrettable in another. This distinction matters because it separates emotional spending psychology from generic money advice and allows the article to examine the hidden passage from relief to regret.

Cognitive closure of the chapter

This chapter establishes that emotions are not exceptions or deviations in financial behavior, but structural components of everyday decision-making. Spending emerges as a situated response to internal states seeking immediate balance, redefining how economic choices should be interpreted. By shifting the focus from moralization to understanding emotional mechanisms, the necessary analytical foundation is created to understand why the pleasure associated with spending repeats itself and how it sets the stage for future tensions. This framing makes it possible to move forward, in the next chapter, to the analysis of the brain’s reward systems that sustain this dynamic.

Chapter 2 — Why Spending Activates Reward Systems in the Brain

The neural architecture of reward

The act of spending money is not processed by the brain as a neutral decision. It activates neural systems associated with reward, originally shaped to reinforce adaptive behaviors such as eating, social bonding, and environmental exploration. These systems operate through circuits involving structures such as the ventral striatum and the prefrontal cortex, which are responsible for associating actions with sensations of pleasure or relief. When a consumption decision is made, especially in contexts of immediate choice, these circuits may be activated even before conscious evaluation of the financial consequences.

Research in neuroeconomics indicates that the expectation of reward is sufficient to generate significant neural activation, regardless of the objective value involved. The mere act of anticipating a purchase can produce brain responses similar to those observed in other reward-seeking behaviors. This helps explain why spending decisions are often accompanied by positive sensations, even if brief, and why these sensations can become a decisive factor at the moment of choice (Knutson & Bossaerts, 2007).

Dopamine and anticipation of pleasure

Dopamine plays a central role in this process. Contrary to the popular interpretation that associates dopamine with pleasure itself, scientific literature describes its primary function as signaling expectation and motivation. It acts as a marker that directs behavior toward stimuli perceived as rewarding. In the context of consumption, dopamine is released primarily during the anticipation phase of a purchase, not necessarily after its completion.

This mechanism explains why the impulse to spend may be stronger before acquisition than the satisfaction that follows. Financial decisions become guided by a system that privileges the present moment, reinforcing choices that promise immediate relief or excitement. Studies show that individuals exposed to consumption stimuli, such as promotions or personalized offers, exhibit greater activation in brain areas associated with reward, even when they rationally recognize that the purchase is unnecessary (Knutson, Rick, Wimmer, Prelec, & Loewenstein, 2007).

Symbolic reward and the meaning of consumption

The reward system does not respond only to material benefits. It is sensitive to symbolic rewards such as status, belonging, and self-image. Products and experiences carry social meanings that enhance their ability to activate emotional responses. Thus, spending money may function as a way to affirm identity, reduce insecurity, or signal belonging to a particular group.

This symbolic aspect of consumption is widely explored in commercial and digital environments. Marketing strategies associate products with narratives of success, self-care, or recognition, reinforcing the emotional activation of decision-making. The pleasure derived from spending, in this case, is not restricted to the acquired object, but to the meaning attributed to it. This dynamic aligns with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), which observes how money intertwines with subjective constructions of value and identity.

The imbalance between fast and deliberative systems

Financial decision-making involves the interaction between fast and deliberative cognitive systems. The fast, automatic, and emotional system responds promptly to reward stimuli, while the deliberative system evaluates costs, benefits, and future impacts. In situations of impulsive spending, the reward system tends to temporarily override the reflective system.

This imbalance does not occur due to a permanent individual failure, but because of structural characteristics of brain functioning. Under cognitive load, stress, or fatigue, the capacity of the deliberative system to modulate impulses decreases. As a result, decisions guided by immediate reward become more likely. Research in behavioral economics indicates that this asymmetry is particularly relevant in contexts of recurring consumption, where decisions are made repeatedly without time for deep reassessment.

The intensification of stimuli in modern environments

Contemporary consumption environments amplify the activation of reward systems. Digital platforms, personalized notifications, and simplified purchasing interfaces reduce friction and accelerate the cycle of anticipation and decision. Each stage of the process is designed to maximize the positive emotional response associated with the act of consuming.

Research reports in consumer behavior observe that the combination of algorithmic personalization and instant access increases the likelihood of decisions guided by emotional reward, especially during moments of psychological vulnerability. Spending ceases to be merely a response to a concrete need and becomes integrated into routines of everyday emotional regulation, reinforcing patterns of repetition.

Implications for understanding recurring spending

By understanding why spending activates reward systems in the brain, it becomes possible to interpret financial behavior beyond moral categories such as self-control or discipline. The pleasure associated with spending emerges from neuropsychological mechanisms that privilege anticipation and immediate relief. These mechanisms are universal, although modulated by social context, gender, and individual experience.

This structural reading helps explain why consumption decisions are repeated even in the face of later regret. The reward system does not operate with long-term memory of consequences, but with immediate signals of perceived value. This characteristic sets the stage for understanding, in the following chapters, how consumption comes to be used as a recurring tool of emotional regulation and why this may generate internal tensions over time.

Cognitive closure of the chapter

This chapter demonstrated that the pleasure associated with spending is not accidental, but the result of activating brain reward systems guided by anticipation and the symbolic meaning of consumption. By privileging immediate stimuli, these systems influence everyday financial decisions before rational evaluation of future costs. This understanding is fundamental for advancing the analysis of how consumption begins to function as a mechanism of emotional relief and why initial satisfaction often gives way to ambiguous feelings later, a theme that will be further explored in the next chapter.

Chapter 3 — Emotional relief, dopamine, and the logic of immediate pleasure

Relief as a short-term psychological response

The pleasure associated with spending does not manifest only as satisfaction or excitement. In many contexts, it takes the subtler form of emotional relief. This relief does not require euphoria; a momentary reduction of an uncomfortable internal state, such as anxiety, frustration, or a sense of loss of control, is sufficient. Emotional psychology describes this process as short-term affect regulation, in which the individual seeks to restore internal balance in response to aversive stimuli.

Within this framework, consumption functions as an instrumental response to negative emotional states. The decision to spend does not need to be accompanied by explicit enthusiasm to fulfill its psychological function. The simple act of acting, choosing, and completing a purchase can produce a sense of temporary closure of internal tension. Studies in behavioral psychology indicate that behaviors capable of reducing immediate discomfort tend to be reinforced, regardless of their future effects (Gross, 2015).

Dopamine, predictability, and repetition

Dopamine plays a central role in this relief mechanism. As discussed in the previous chapter, its primary function relates to anticipation and motivation, not to final reward. In the context of emotional relief, dopamine signals predictability: the brain learns that a certain behavior is capable of reducing discomfort in the short term. This predictability is sufficient to reinforce the pattern, even when the resulting satisfaction is limited or fleeting.

Research in behavioral neuroscience suggests that the dopaminergic system responds strongly to situations in which the individual perceives a clear route between action and reduction of tension. Consumption offers exactly this structure: stimulus, choice, action, and rapid resolution. This sequence creates a closed cycle that favors repetition. Over time, the brain begins to associate specific emotional states with the impulse to consume, regardless of the objective utility of the expenditure.

This mechanism helps explain why financial decisions guided by relief tend to repeat themselves even when accompanied by later regret. The neural system involved does not operate with retrospective evaluation of consequences, but with the memory of relief experienced at the moment of action. This temporal asymmetry is fundamental for understanding the persistence of the behavior.

Immediate pleasure and the compression of decision time

The emotional relief associated with consumption operates within a specific temporal logic: the compression of the future. When cognitive focus is concentrated on the immediate reduction of discomfort, medium- and long-term consequences become cognitively distant. Behavioral economics describes this phenomenon as hyperbolic discounting, in which immediate rewards are disproportionately valued relative to future benefits.

In this context, immediate pleasure does not need to be intense to be decisive. Its advantage lies in temporal proximity. Classic studies demonstrate that individuals tend to prefer smaller, immediate rewards over larger, delayed rewards, especially under emotional stress (Laibson, 1997). Applied to consumption, this pattern explains why small purchases may seem justifiable at the moment, even when they accumulate into significant financial impacts.

This process does not occur in isolation. It is reinforced by environments that reduce friction and accelerate decisions, such as digital platforms and instant payment systems. By eliminating intervals for reflection, these environments intensify the logic of immediate pleasure, making emotional relief even more accessible.

This point is important because emotional spending becomes stronger when the distance between feeling and buying becomes shorter. A purchase that might have required more reflection in a physical environment can become almost immediate in a digital one, especially when payment details are saved, offers are personalized, and the emotional promise of relief appears before the financial consequence feels real.

Consumption as a tool of self-regulation

Within this framework, consumption can be understood as an informal tool of emotional self-regulation. It does not replace conscious coping strategies, but functions as a quick and available solution. This role is not pathological by definition; it becomes problematic when it begins to be used in a recurring and exclusive manner.

Research in emotion psychology indicates that regulation strategies focused solely on suppression or immediate relief tend to produce side effects over time, such as increased guilt or reduced perception of control. In the financial context, these effects manifest as tension between momentary pleasure and subsequent evaluation of spending. This tension sets the stage for feelings of dissonance, which will be explored in the following chapters.

Understanding consumption as an emotional tool aligns with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by reinforcing that financial decisions are often adaptive responses to internal states, not simple planning failures.

Limits of relief and accumulation of tension

Although effective in the short term, the relief provided by consumption has structural limits. Its transient nature requires repetition to maintain the same effect, creating increasingly frequent cycles. In addition, the discrepancy between immediate relief and later consequences may generate an accumulation of emotional tension. The individual begins to experience not only the initial discomfort, but also secondary feelings related to the spending behavior itself.

Studies on financial well-being observe that individuals who use consumption as their primary way of dealing with negative emotions tend to report greater financial stress over time, even when the volume of spending is not objectively high. This suggests that the emotional impact of the pattern may be as relevant as its material impact (Federal Reserve Board, 2023).

Cognitive closure of the chapter

This chapter showed that the pleasure associated with spending often takes the form of emotional relief, mediated by dopaminergic mechanisms that privilege predictability and temporal proximity. This relief does not depend on lasting satisfaction, but on the momentary reduction of discomfort, which explains its strength and repetition. Operating within a short-term logic, consumption begins to function as a recurring tool of emotional self-regulation, setting the stage for internal tensions that emerge when rational evaluation returns. This dynamic is essential for understanding, in the next chapter, how consumption can transform into a systematic regulator of emotional states.

Chapter 4 — When consumption begins to regulate emotional states

From isolated episode to recurring pattern

The use of consumption as a response to emotional states generally does not occur as an isolated or conscious event. It tends to establish itself gradually, based on repeated experiences in which spending produces momentary relief or a sense of control. Over time, this linkage between emotion and action no longer requires deliberate reflection and begins to operate as an automatic pattern. The decision to consume emerges as a learned response, triggered whenever certain internal states are activated.

Learning psychology describes this process as instrumental conditioning: behaviors that reduce discomfort tend to be reinforced and repeated. In the financial context, consumption offers a quick, predictable, and socially accepted response for dealing with diffuse emotions such as frustration or insecurity. This predictability contributes to the incorporation of the behavior into everyday repertoire, even when its material consequences are not fully evaluated.

Consumption and emotional identity

As consumption begins to perform a regulatory function, it ceases to be merely a punctual action and becomes integrated into how the individual deals with their own emotions. Spending may assume identity-related meanings, becoming associated with self-care, deservingness, or compensation. In these situations, the financial decision responds not only to a momentary emotional stimulus, but to an internal narrative about who the person is and how they should treat themselves.

Research in social psychology indicates that consumption practices often intertwine with identity construction, functioning as means of expressing values, belonging, and self-esteem. This interweaving expands the emotional role of spending, making it more resistant to rational revision. Questioning the behavior implicitly becomes questioning one’s own personal narrative. This mechanism helps explain why patterns of emotional consumption persist even in the face of signs of financial discomfort.

This dynamic connects to broader discussions presented in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by highlighting how money and identity mutually influence one another. It also opens a natural bridge to women’s money stories and emotional spending, because personal narratives often determine whether spending is interpreted as care, compensation, weakness, or relief.

The social normalization of emotional consumption

Consumption as an emotional regulator does not develop solely at the individual level. It is widely normalized by cultural practices, market discourses, and digital environments. Expressions such as “shopping to feel better” or “treating yourself” reinforce the association between spending and emotional care. This normalization reduces the perceived risk of the behavior, framing it as a legitimate response to common emotional states.

Contemporary consumer environments often reinforce this association by presenting buying as an accessible solution for coping with stress, fatigue, and everyday overload. This is why the emotional dimension of spending also connects with emotional spending under stress, where uncertainty and psychological pressure make financial decisions feel more urgent and less reflective.

This symbolic environment creates conditions in which individuals encounter little social friction in using spending as an emotional strategy. On the contrary, the behavior is often reinforced by messages that associate consumption with immediate well-being.

When this emotional normalization enters digital checkout environments, the pattern can become even more difficult to notice. Payment models that separate the feeling of buying from the feeling of paying may make emotional spending appear smaller, easier, or less consequential in the moment. This is why the psychology of emotional spending also connects with the hidden costs of Buy Now, Pay Later financing, where relief, convenience, and delayed cost perception can converge.

Emotional regulation and reduced cost sensitivity

When consumption begins to operate as an emotional regulator, the individual’s attention shifts from financial cost to immediate psychological effect. Monetary value ceases to be the primary decision criterion, giving way to the perceived effectiveness of spending in producing relief. This shift does not imply ignorance of cost, but a different prioritization at the moment of choice.

Behavioral economics describes this phenomenon as reduced cost salience, in which future financial impact is cognitively attenuated. Studies show that, in emotionally charged contexts, individuals tend to underestimate accumulated costs and overestimate immediate benefits, even when they possess adequate information about their finances (Gennaioli, Shleifer, & Vishny, 2018).

This process contributes to the repetition of the behavior, since negative cost feedback is not immediately perceived. Emotional regulation occurs in the present, while financial consequences manifest in a diffuse and delayed manner.

The cycle of functional dependence

As consumption consolidates itself as an emotional regulator, a cycle of functional dependence forms. Uncomfortable emotional states trigger the impulse to spend; spending produces temporary relief; relief reinforces the pattern; and repetition increases the likelihood of future recurrence. This cycle does not require high volumes of consumption to become established. Small, frequent expenditures can fulfill the same psychological function.

Research on financial well-being indicates that individuals who report using consumption as their primary way of dealing with negative emotions are more likely to experience persistent financial stress, regardless of income level. The Report on the Economic Well-Being of U.S. Households observes that the perception of financial fragility is strongly associated with how everyday decisions are emotionally experienced, not only with the objective balance of resources (Federal Reserve Board, 2023).

This finding suggests that the impact of emotional consumption is not limited to the budget, but affects the subjective relationship with money, amplifying feelings of insecurity over time.

Cognitive closure of the chapter

This chapter showed how consumption can cease to be a punctual response to emotions and begin to operate as a systematic regulator of emotional states. By integrating into identity, social norms, and decision environments, spending assumes a psychological function that relativizes cost perception and favors repetition. This process creates functional cycles that are difficult to interrupt, not because of lack of awareness, but because of the immediate effectiveness of the relief produced. Understanding this dynamic is essential for advancing, in the next chapter, to the analysis of the internal tensions that emerge when initial relief gives way to rational evaluation and financial regret.

Chapter 5 — Cognitive Dissonance and the Emergence of Financial Regret

The return of rational evaluation

After the moment of relief or immediate pleasure described in the previous chapters, the financial decision tends to be reassessed under a different cognitive frame. As emotional intensity decreases, the individual regains greater capacity for deliberate reflection and begins to confront the completed spending with their goals, values, and financial constraints. It is within this temporal shift that financial regret emerges.

Cognitive psychology describes this process as cognitive dissonance: the discomfort generated by the coexistence of two incompatible cognitions, such as “spending made me feel better” and “this spending was not consistent with what I wanted for my finances.” This discomfort does not arise because the decision was irrational at its origin, but because it was made under a set of emotional priorities that is no longer active at the time of later evaluation (Festinger, 1957).

Regret, therefore, is not simple retrospective disapproval, but a signal of transition between two distinct cognitive modes. It marks the point at which the emotional system gives way to the reflective system, reintroducing long-term criteria that had been temporarily suspended.

Regret as a secondary emotional experience

Unlike pleasure or immediate relief, financial regret is a secondary emotion. It does not emerge directly from the act of spending, but from the later interpretation of that act in light of expectations and internal norms. This characteristic helps explain why regret tends to be more enduring than the pleasure that preceded it.

Research in economic psychology indicates that secondary emotions such as guilt and regret are strongly associated with counterfactual evaluation—that is, the comparison between what occurred and what could have occurred if a different choice had been made. This type of evaluation intensifies negative emotional load, because it introduces a sense of missed opportunity or personal failure, even when the original decision met a legitimate emotional need at the time it was made (Zeelenberg & Pieters, 2007).

In the financial context, this dynamic is particularly relevant because money carries a strong moral dimension. Spending in a way perceived as inappropriate may be interpreted not only as a practical mistake, but as a sign of lack of self-control or responsibility, amplifying the emotional impact of regret.

The asymmetry between pleasure and regret

A central aspect of financial regret is its asymmetry relative to the pleasure that precedes it. While immediate pleasure is brief and diffuse, regret tends to be clearer and more persistent. Studies in behavioral economics suggest that losses and negative outcomes exert a more intense psychological impact than equivalent gains, a phenomenon known as loss aversion (Kahneman & Tversky, 1979).

This asymmetry contributes to the perception that the spending “was not worth it,” even when momentary pleasure was real. Emotional memory privileges later discomfort, reinforcing the sense of error. However, this retrospective reading ignores the original emotional context of the decision, creating a simplified narrative that pits irrational pleasure against correct reason.

This simplification fuels cycles of self-criticism in which the individual begins to interpret past decisions as moral failures rather than situated responses to specific emotional states. This process connects to broader discussions presented in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by showing how emotions shape not only choices, but also later interpretations of those choices.

Cognitive strategies for dissonance reduction

In the face of the discomfort of regret, individuals tend to adopt cognitive strategies to reduce dissonance. These strategies may include rationalizations (“I deserved it”), minimizing the impact (“it wasn’t that much”), or shifting responsibility (“the context led me to it”). These responses do not eliminate regret, but make it psychologically more tolerable.

The literature in social psychology observes that such strategies are common and adaptive, because they reduce excessive emotional suffering. However, when applied repeatedly, they may prevent full integration of the experience. Spending remains associated with both relief and regret, without the individual being able to work through the tension between these two dimensions.

This impasse contributes to repetition of the pattern: consumption continues to be used as an emotional regulator, while regret is treated as an isolated episode, not as part of a structural dynamic. The lack of integration between pleasure and regret prevents the construction of a coherent financial narrative over time.

Regret as a signal, not a failure

Interpreting financial regret exclusively as a personal error obscures its psychological function. Regret acts as a signal that different value systems are in conflict: a system oriented toward immediate relief and a system oriented toward long-term goals. This conflict does not indicate pathology, but complexity.

When repeated regret becomes tied to revolving balances, minimum payments, or high-interest pressure, the emotional pattern moves beyond a single purchase and begins to affect financial stability. At that point, the discussion naturally extends to the hidden price of credit card debt for women, where emotional relief, delayed cost, and debt pressure can become part of the same cycle.

Cognitive closure of the chapter

This chapter showed that financial regret emerges from the dissonance between the immediate emotional relief of spending and later rational evaluation. This secondary emotion is intensified by cognitive asymmetries and by the moral weight associated with money, making it more persistent than the pleasure that preceded it. By understanding regret as a signal of conflict between value systems, rather than a simple individual failure, it becomes possible to move forward to the analysis of the moral emotions that settle in this interval, a theme that will be deepened in the next chapter.

Chapter 6 — Guilt, shame, and the moral narrative around money

Moral emotions and financial evaluation

When financial regret sets in, it rarely remains an isolated emotion. It is often accompanied by feelings of guilt and shame, which introduce a moral dimension into the interpretation of spending. Unlike regret, which is linked to evaluating a specific decision, guilt and shame involve judgments about the self. The focus shifts from merely “I made an inadequate choice” to including “there is something wrong with me for having made that choice.”

Moral psychology distinguishes guilt and shame based on the object of evaluation. Guilt is associated with the action and with violating internal or social norms, while shame falls on identity, producing a sense of personal inadequacy. In the financial context, this distinction is relevant because money occupies a central place in social narratives about responsibility, self-control, and individual worth. Spending in a way perceived as excessive or inappropriate may be interpreted not only as a practical mistake, but as a moral failure.

The social construction of financial morality

The association between money and morality is neither natural nor inevitable; it is socially constructed over time. Cultural discourses often link financial success to virtue and economic hardship to individual failures. This narrative reinforces the idea that financial decisions reflect character, discipline, and merit, obscuring emotional and contextual factors that influence behavior.

Studies in economic sociology observe that moral norms around money are internalized early, shaping how individuals evaluate their own financial choices. This internalization causes emotions such as guilt and shame to arise automatically when decisions do not align with the ideal of financial self-control, even when those decisions respond to legitimate emotional needs at the moment they were made.

Institutional reports on financial well-being indicate that feelings of guilt and shame about money are widespread across income levels and educational backgrounds. The Report on the Economic Well-Being of U.S. Households observes that many people avoid discussing financial difficulties precisely because they associate those difficulties with personal failure, which intensifies emotional isolation (Federal Reserve Board, 2023).

Shame and the silencing of financial experience

Shame has a particularly corrosive effect because it tends to produce silence. Unlike guilt, which can motivate repair or reflection, shame encourages concealment and withdrawal. In the financial sphere, this translates into avoiding looking at statements, delaying decisions, or not sharing concerns with others. Financial behavior becomes accompanied by constant tension, in which money becomes a source of emotional discomfort.

Research in social psychology indicates that shame reduces the capacity to learn from experience because it shifts focus from the situation to negative self-evaluation. Instead of integrating the spending episode into a broader understanding of one’s financial behavior, the individual begins to treat it as proof of personal inadequacy. This process makes it harder to process the experience and favors repetition of patterns, because the dominant emotion becomes something to avoid rather than understand.

This dynamic helps explain why patterns of emotional consumption can persist even when they produce subjective suffering. Spending continues to function as an emotional regulator, while the shame associated with regret remains without conscious elaboration.

Guilt, self-control, and cycles of punishment

Financial guilt, in turn, tends to manifest as a demand for future self-control. After a spending episode accompanied by guilt, individuals may adopt internal narratives of punishment, such as rigid promises of restriction or self-censure. These narratives reinforce the moralization of the decision, turning money into a field of discipline and constant surveillance.

Behavioral economics observes that strategies based exclusively on punishment tend to be unstable over time. Under emotional load or stress, rigid demands for self-control may fail, reactivating the cycle of consumption and regret. This back-and-forth between indulgence and punishment intensifies the emotional charge of the relationship with money without resolving the underlying conflict between immediate relief and long-term goals.

This reading aligns with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by showing how rigid moral narratives can obscure the emotional mechanisms that structure recurring financial decisions.

Accumulated emotional weight

Over time, the repetition of episodes of guilt and shame around money can produce accumulated emotional weight. Money ceases to be merely a functional resource and becomes a constant source of anxiety and self-criticism. This weight is not necessarily related to spending volume or debt level, but to how financial decisions are emotionally interpreted.

Research on mental health and finances indicates that persistent feelings of financial shame are associated with greater psychological stress and lower sense of autonomy, even when objective indicators of financial stability are reasonable. This suggests that the emotional impact of moralizing money can be as relevant as its material effects.

Cognitive closure of the chapter

This chapter showed how guilt and shame introduce a moral narrative into the relationship with money, turning financial decisions into judgments about personal worth. These emotions amplify the impact of regret, produce silence, and foster cycles of punishment that do not integrate the original emotional experience of spending. By understanding the moral dimension of these emotions, it becomes possible to move forward to the analysis of how environments and external structures amplify these emotional responses, a theme that will be deepened in the next chapter.

Chapter 7 — How the consumption environment amplifies emotional responses

Choice architectures and emotional stimuli

Financial decisions do not happen in a psychological vacuum. They unfold within environments carefully structured to direct attention, reduce friction, and intensify emotional responses. Behavioral economics describes these contexts as choice architectures: configurations that influence decisions without formally restricting individual freedom. In the contemporary consumption environment, these architectures are designed to favor fast, emotionally charged, and minimally reflective responses.

Elements such as visual layout, highlighted offers, artificial scarcity, and urgency language act as emotional triggers. They not only facilitate decisions, but amplify activation of the reward systems described in earlier chapters. Research in economic psychology indicates that environments with a high density of emotional stimuli tend to shift the individual’s focus from evaluating consequences to the immediate experience of choice (Thaler & Sunstein, 2008).

This shift is particularly relevant in contexts of stress or cognitive fatigue. When mental resources are reduced, the environment plays an even more decisive role, amplifying preexisting emotional predispositions and making consumption an accessible response to uncomfortable internal states.

Digitization, speed, and the compression of decision time

Digitization has decisively intensified the power of the consumption environment over emotional responses. Digital platforms operate at high speed, shortening the interval between desire, decision, and action. This shortening of decision time reduces opportunities for emotional and rational reassessment, favoring choices driven by impulse and by anticipation of immediate relief.

Studies on consumer behavior observe that eliminating intermediate steps in the purchasing process significantly increases the likelihood of impulsive decisions. One-click payments, automatic data storage, and personalized notifications turn the financial decision into an almost automatic gesture. Research in behavioral marketing indicates that the less effort required to complete a purchase, the greater the influence of momentary emotional states on the final decision (Ariely, 2008). This mechanism also connects with the hidden cost of credit card convenience, because reduced friction can make the emotional reward of spending arrive before the real cost becomes visible.

The same mechanism also helps explain why digital installment options can feel emotionally lighter than traditional debt. When a purchase is divided into smaller payments at checkout, the immediate reward remains visible while the full cost becomes psychologically distant. This makes Buy Now, Pay Later an important continuation of this discussion, not because it creates emotional spending alone, but because it can make emotionally driven purchases feel easier to justify.

Language, narrative, and emotional legitimation of spending

Beyond speed and reduced friction, the consumption environment operates through language and narrative. Terms such as “deserved,” “self-care,” and “reward” frame spending as a legitimate response to effort, frustration, or emotional overload. This language does not create emotions from scratch, but legitimizes emotions that already exist, offering a symbolic frame that favors the decision to consume.

Social psychology observes that narratives play a central role in emotional regulation because they help individuals assign meaning to their own actions. When spending is narrated as self-care or recognition, it integrates more easily into an individual’s identity, reducing internal conflict at the moment of choice. This symbolic framing weakens risk perception and delays the emergence of regret described in earlier chapters.

This dynamic aligns with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by showing how money, emotion, and cultural narrative intertwine in the construction of everyday financial behavior.

The environment as a continuous emotional mediator

Viewed integratively, the consumption environment acts as a continuous emotional mediator between internal states and financial decisions. It not only responds to an individual’s emotions, but anticipates, organizes, and intensifies them. By offering fast and symbolically legitimized solutions for everyday discomfort, the environment reduces the need to reflect on non-monetary alternatives for emotional regulation.

Research in consumer psychology indicates that highly stimulating environments increase reliance on external cues for decision-making, reducing an individual’s sensitivity to the accumulated cost of choices (Gennaioli, Shleifer, & Vishny, 2018). Consumption ceases to be merely a punctual response and becomes integrated into recurring emotional routines, sustained by the predictability of the environment.

Institutional reports observe that consumers often report a sense of loss of financial control in complex digital environments, even when they have adequate information about their finances. This perception suggests that the environment’s impact is more emotional than informational, reinforcing short-term decision patterns (Federal Reserve Board, 2023).

Limits of an individualistic reading of financial behavior

The environmental amplification of emotional responses challenges readings that attribute financial behavior exclusively to individual willpower. Although decisions are made by individuals, they occur within structures that direct attention, emotion, and action. Ignoring this context results in incomplete analyses that overestimate decision autonomy and underestimate systemic influence.

This recognition does not eliminate personal agency, but reinserts it into a more realistic framework in which emotions and environments interact continuously. Emotional consumption emerges at the intersection between internal states and external architectures, and it is at this point that patterns consolidate and become difficult to break.

Cognitive closure of the chapter

This chapter showed how the consumption environment amplifies emotional responses by organizing choices, accelerating decisions, and legitimizing spending as an immediate solution for everyday discomfort. By acting as a continuous emotional mediator, the environment reduces friction, compresses decision time, and weakens perception of future cost. Understanding this structural amplification is essential for advancing, in the next chapter, to the analysis of how these dynamics affect groups unequally and why gender matters in the emotional experience of spending.

Chapter 8 — Gender differences in the emotional experience of spending

Financial socialization and the emotional construction of money

The emotional experience of spending is not shaped only by individual personality. It is also influenced by socialization, household roles, cultural expectations, and the meanings attached to money over time. For many women, money may be associated with responsibility, care, security, and predictability, while personal spending can be framed as an exception, indulgence, or temporary deviation from those priorities.

Research in social psychology and gender studies indicates that women internalize norms of financial prudence and vigilance over their own economic behavior more intensely. This internalization is not limited to explicit rules, but operates as an emotional backdrop that precedes the decision to spend. The pleasure associated with personal consumption, when it occurs, is often accompanied by ambiguous feelings such as the need for justification or anticipation of guilt (Baker & Gentry, 2014).

This pattern does not stem from biological differences, but from persistent social constructions that link feminine worth to the ability to manage resources responsibly and altruistically. As a result, the emotional experience of spending begins already tense, even before any financial consequence becomes visible.

Social judgment and emotional self-censorship

Beyond early socialization, the emotional experience of spending is shaped by implicit social judgment. Women tend to be evaluated more harshly when they make expenditures considered superfluous or oriented toward personal pleasure. This judgment does not need to be externally stated to have an effect; it is often anticipated and internalized, operating as emotional self-censorship.

Studies in the sociology of consumption show that similar spending practices receive different interpretations depending on gender. While men’s spending tends to be framed as individual choices or expressions of autonomy, women’s spending is more readily associated with irresponsibility or lack of self-control (Dittmar, 2005). This asymmetry increases the emotional load associated with consumption, making financial regret more intense and persistent among women.

Anticipation of judgment contributes to experiencing emotional spending as a symbolic transgression. Even when the amount is small or compatible with the financial situation, the decision can activate internal narratives of disapproval. This reinforces the cycle described in earlier chapters, in which immediate pleasure is quickly replaced by moral emotions such as guilt and shame.

Money, care, and the emotional hierarchy of spending

For many women, money is deeply intertwined with practices of care. Spending on family, health, education, and household maintenance is emotionally legitimized and perceived as a priority. In contrast, spending oriented toward one’s own well-being tends to occupy a lower place in the emotional hierarchy of the budget. This hierarchy is not necessarily conscious, but it guides how decisions are felt and evaluated.

Feminist economics observes that the centrality of care in women’s financial experience produces an ambivalent relationship with personal consumption. Spending may offer genuine emotional relief, but it can also activate internal narratives of guilt for diverting resources from responsibilities perceived as more legitimate (Folbre, 2001). This ambivalence intensifies the tension between pleasure and regret, making emotional consumption a particularly charged territory.

This dynamic helps explain why women often report emotional discomfort even in stable financial situations. The issue is not spending itself, but the emotional interpretation that accompanies it, shaped by enduring social expectations.

Security, risk, and financial anxiety

Research in financial behavior indicates that women, on average, report greater concern about long-term security and greater aversion to financial risk. This orientation directly influences the emotional experience of spending. Decisions oriented toward immediate pleasure may be experienced as a symbolic threat to a carefully built foundation of stability, intensifying internal conflict.

Empirical studies suggest that this difference is associated with more unstable economic trajectories, career interruptions, and greater shared financial responsibility across life. As a result, emotional spending may represent not merely a punctual decision, but a temporary rupture in a constant posture of vigilance and risk anticipation (Lusardi & Mitchell, 2014).

This context amplifies the emotional intensity of regret when spending is perceived as misaligned with expectations of control and responsibility. It also connects with scarcity mindset and women’s wealth-building behavior, because the feeling of having little room for error can make even ordinary spending feel emotionally risky.

Accumulated emotional consequences

The combination of differentiated socialization, moral judgment, and an orientation toward security produces cumulative emotional consequences. Over time, money ceases to be merely a functional instrument and begins to act as a symbolic mirror of personal worth. Financial decisions are interpreted as indicators of competence, care, and emotional maturity.

In this scenario, emotional consumption takes on disproportionate weight. The pleasure of spending is experienced with caution and justification; regret, with amplified intensity. This pattern does not reflect individual fragility, but social structures that distribute emotional expectations unevenly across genders. The emotional experience of money thus becomes a field of continuous tension in which relief and self-censorship coexist.

This does not mean that women are naturally more emotional with money or less capable of rational financial decisions. The point is structural: when responsibility, care, security, and self-restraint are repeatedly attached to women’s financial roles, ordinary spending can carry a heavier emotional interpretation. The same purchase may therefore be experienced not only as a financial decision, but as a test of responsibility, deservingness, and control.

This reading aligns with analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by showing how financial emotions are shaped by gender, social context, and persistent cultural narratives.

Cognitive closure of the chapter

This chapter showed that gender differences in the emotional experience of spending emerge from socialization processes, moral judgment, and durable expectations of care and security. For many women, personal consumption is marked by emotional ambivalence in which relief and self-censorship coexist intensely. Understanding these differences does not mean essentializing behaviors, but recognizing structures that shape the relationship with money over time. This recognition sets the stage for the final chapter, which analyzes how to recognize emotions without turning them into punishment, closing the cognitive arc of the article.

Chapter 9 — Recognizing Emotions Without Turning Decisions Into Punishment

Emotional recognition as an interpretive step

Across the previous chapters, it has become clear that emotional consumption is not an episodic deviation, but part of a psychological system that seeks to regulate internal states in specific contexts. The challenge that emerges at the close of this arc is not to eliminate emotions from financial decision-making, but to recognize them without automatically converting them into punitive judgments. Recognizing emotions, in this sense, is an interpretive process, not a moral evaluation.

Contemporary psychology distinguishes emotional recognition from emotional reactivity. Recognition involves identifying and naming internal states, understanding their role at the moment of decision. Reacting, by contrast, involves automatic responses of guilt, shame, or self-censorship. Research indicates that the absence of recognition tends to intensify negative secondary reactions, while conscious identification of emotions reduces the need for later symbolic punishment (Barrett, 2017).

In the financial context, this distinction is crucial. When emotions are recognized as a legitimate part of the decision-making process, spending stops being interpreted exclusively as failure. It begins to be understood as a situated response to a specific emotional need, even if it carries material consequences that deserve later analysis.

From moralization to process understanding

Turning financial decisions into personal punishment is strongly associated with the moralization of money. As discussed earlier, social narratives link financial self-control to virtue and deviations to character flaws. This framing favors punitive responses in the face of regret, such as harsh self-criticism or rigid promises of future compensation.

Behavioral economics observes that punishment-based approaches tend to produce unstable cycles. Self-censorship intensifies the emotional load associated with money, increasing the likelihood that future decisions will be made under stress or avoidance. Studies in motivation psychology indicate that internal environments marked by punishment reduce the capacity to learn from experience because they shift focus from understanding the process to defending identity (Deci & Ryan, 2000).

By replacing moralization with process understanding, financial decisions can be reinterpreted without denying their consequences. Recognizing the role of emotions does not absolve the material impact of spending, but prevents it from being transformed into proof of personal inadequacy. This shift in framing changes how past experiences inform future decisions.

This reading connects to analyses developed in The Psychology of Money: Why We Spend, Save, and Struggle With Debt and Financial Decisions (Article #21, Cluster 2), by emphasizing that understanding emotional patterns is a precondition for interpreting financial decisions in an integrated way.

Integration between emotion and rational evaluation

Recognizing emotions without punishment does not mean abandoning rational evaluation. On the contrary, it creates conditions for evaluation to occur in a less defensive and more informative way. When the immediate reaction of guilt is softened, individuals can examine the decision with greater clarity, identifying circumstances, triggers, and effects without resorting to simplifying narratives.

Research in cognitive psychology suggests that integrating emotion and reason supports adaptive learning. Rather than eliminating emotions from the decision-making process, this integration allows them to be considered as contextual data. Emotional spending comes to be seen as part of an observable pattern, not as an isolated event or moral failure (Gross, 2015).

This integration also reduces the likelihood of the punishment-and-indulgence cycles described in earlier chapters. By understanding the role of emotional relief at the moment of decision, individuals can contextualize later regret without amplifying it. Money ceases to be a field of constant judgment and becomes an object of relational analysis.

Human limits and interpretive autonomy

A central aspect of this framework is recognizing human limits. Financial decisions are made under cognitive, emotional, and contextual constraints. Admitting these limits does not mean relinquishing autonomy, but redefining it in a more realistic way. Interpretive autonomy lies in the capacity to understand one’s own behavior within those limits, not in the expectation of absolute control.

Discourses of “perfect discipline” in personal finance often ignore the emotional complexity of everyday life. Pressure for total control can increase financial anxiety and feelings of inadequacy rather than promote emotional stability. This is why a less punitive reading is not a softer interpretation, but a more realistic one.

Recognizing emotions, therefore, is not a concession, but an interpretive tool. It allows financial decisions to be understood as part of a trajectory, not as isolated tests of character.

Building a non-punitive financial narrative

At the end of this article’s cognitive arc, it becomes possible to see that the relationship between pleasure, regret, and emotion does not need to culminate in punishment. Building a non-punitive financial narrative involves integrating past experiences without turning them into permanent sources of self-censorship. This narrative recognizes the emotional function of spending, evaluates its consequences, and remains open to future revisions.

This approach does not promise the elimination of regret, but its transformation into information. Regret ceases to be a sign of failure and becomes an indicator of tension between short-term needs and long-term goals. This tension, when recognized, can be observed without moral amplification.

For the reader, this final step also opens a broader path through the HerMoneyPath ecosystem. Emotional spending can be understood first as a psychological pattern, then as a behavior shaped by digital checkout systems, credit convenience, and debt structures. That is why the natural continuation of this article is not more self-blame, but a clearer understanding of how emotional relief can interact with modern credit tools and long-term financial pressure.

Cognitive closure of the chapter

This chapter showed that recognizing emotions in financial decisions does not require turning them into personal punishment. By replacing moralization with process understanding, it becomes possible to integrate pleasure and regret as parts of the same human dynamic. This integration restores interpretive autonomy to financial experience, allowing decisions to be analyzed within their emotional and temporal contexts. In closing this arc, the article reaffirms that the relationship between money and emotion is not a problem to be eliminated, but a reality to be understood.

Frequently Asked Questions

What is emotional spending?

Emotional spending happens when a purchase is shaped by feelings such as stress, fatigue, anxiety, boredom, sadness, or the desire for comfort. The purchase may feel useful in the moment because it offers quick relief, reward, or a temporary sense of control, even if regret appears later.

Why does spending money feel good at first?

Spending can feel good because buying often activates anticipation, reward, and emotional relief. The brain may respond to the possibility of getting something, feeling better, or solving discomfort quickly. In many cases, the strongest emotional reward happens before or during the purchase, not after the item is owned.

Why do I regret spending money after buying something?

Regret often appears after the emotional intensity of the purchase fades. Once stress, excitement, or urgency decreases, the decision may be reinterpreted through bills, debt, savings goals, personal expectations, or the feeling that the money could have been used differently. This does not always mean the original emotion was false; it means the decision is being evaluated from a different mental state.

Is emotional spending the same as lack of discipline?

No. Emotional spending is not simply a lack of discipline. It is a psychological pattern shaped by stress, reward systems, digital buying environments, personal history, social pressure, and the emotional meaning of money. Discipline may matter, but it is only one part of a much larger decision-making process.

How do digital shopping environments increase emotional spending?

Digital shopping environments can increase emotional spending by reducing friction between desire and purchase. Personalized offers, one-click checkout, limited-time messages, saved payment details, and constant access to online stores can shorten the time available for reflection, especially during moments of stress or fatigue.

Why can emotional spending feel worse for women?

For many women, spending decisions can carry additional emotional weight because money is often tied to care, responsibility, household stability, self-worth, and social judgment. A purchase that feels comforting in the moment may later be judged against expectations of restraint, sacrifice, or responsibility, making guilt or shame more intense.

Can emotional spending lead to debt?

Emotional spending can contribute to debt when small purchases become frequent, when credit cards or Buy Now, Pay Later options make spending feel easier, or when emotional relief becomes tied to repeated borrowing. The issue is not only one purchase, but the pattern that forms when short-term relief is financed through future obligations.

How can financial regret be useful?

Financial regret can be useful when it is treated as information rather than punishment. It may reveal a conflict between short-term emotional needs and longer-term financial goals. Instead of turning regret into shame, it can help identify patterns, triggers, and moments when spending is being used to manage emotional pressure.

Does emotional spending always mean the purchase was wrong?

No. A purchase influenced by emotion is not automatically wrong. All financial decisions involve emotion in some way. The question is whether the purchase fits the person’s broader financial reality, values, obligations, and goals, or whether it repeatedly creates stress, guilt, debt, or loss of control afterward.

How can someone better understand emotional spending patterns?

A helpful first step is to notice the emotional moment before the purchase: stress, fatigue, loneliness, boredom, anxiety, or the desire for reward. The goal is not to punish the emotion, but to understand what the purchase is trying to solve. This makes it easier to separate real needs, temporary relief, and financial choices that may create regret later.

Conclusion

Emotional spending is not simply a moment of weak discipline, impulsiveness, or poor planning. As this article has shown, the pleasure associated with spending and the regret that often follows are part of the same psychological sequence. A purchase may first feel comforting, rewarding, or emotionally useful because it responds to stress, fatigue, anxiety, boredom, or the desire to feel in control. Later, when that emotional intensity fades, the same decision may be reinterpreted through bills, goals, debt, personal expectations, or the pressure to be financially responsible.

This time gap is central to emotional spending psychology. Financial decisions can feel reasonable in one moment and uncomfortable in another because emotion and reflection do not always operate at the same speed. The reward system responds quickly to relief, anticipation, and symbolic meaning, while long-term evaluation often returns afterward. Regret, in this context, is not proof that the original emotion was false; it is a signal that short-term emotional needs and broader financial priorities are competing for attention.

The article also showed that emotional spending does not happen in isolation. Digital shopping environments, personalized offers, frictionless checkout, urgency language, and cultural messages about self-care can intensify the emotional pull of buying. These environments shorten the distance between desire and action, making spending feel easier precisely when stress or exhaustion reduces the space for reflection.

For many women, the emotional experience of spending can also carry additional symbolic weight. Money is often connected to responsibility, care, household stability, self-worth, restraint, and social judgment. This can make ordinary spending decisions feel morally loaded, especially when pleasure is followed by guilt, shame, or self-criticism. Understanding this context helps separate financial awareness from punishment.

Recognizing these dynamics does not mean ignoring financial consequences. It means interpreting them with greater accuracy. Regret can become useful when it is treated as information rather than evidence of personal failure. It can reveal the tension between immediate relief and long-term goals, between self-comfort and financial pressure, between emotional need and structural constraint.

At the end of this analysis, money appears less as a field of moral judgment and more as a space where emotion, context, identity, and expectation constantly interact. By understanding why spending can feel good at first and why regret may follow, women can begin to read their financial decisions with more clarity, less shame, and a deeper awareness of the emotional patterns shaping everyday money choices.

Editorial Note and Disclaimer

This article is for educational and informational purposes only. Its purpose is to explain emotional spending, financial regret, money emotions, consumer behavior, and the psychological patterns that can influence everyday financial decisions.

The analysis draws on concepts from behavioral economics, psychology, neuroeconomics, consumer behavior, and household financial well-being to help readers understand why spending may feel emotionally rewarding in the moment and why regret, guilt, or shame may appear later. The content is intended to offer context and reflection, not to diagnose behavior, provide therapy, or replace professional mental health, financial, legal, or investment guidance.

Financial decisions are personal and depend on each reader’s income, obligations, debt level, savings, family responsibilities, emotional context, financial goals, planning horizon, and risk tolerance. Readers should evaluate their own circumstances carefully and, when necessary, consult qualified professionals such as financial planners, credit counselors, legal advisors, tax professionals, or licensed mental health professionals.

Nothing in this article should be interpreted as individualized financial advice, investment advice, legal advice, psychological counseling, debt counseling, or a recommendation to buy, avoid, finance, borrow, save, invest, or make any specific financial decision. The article does not guarantee financial results, emotional outcomes, debt reduction, savings growth, investment performance, or changes in personal financial behavior.

HerMoneyPath does not assume responsibility for financial losses, debts, missed payments, late fees, interest charges, credit score impacts, investment losses, legal consequences, emotional distress, purchasing decisions, borrowing decisions, budgeting decisions, or any other damages or outcomes that may result from actions taken based on the information presented in this content.

Each reader is responsible for her or his own financial choices and for seeking appropriate professional support before making decisions involving credit, debt, spending, saving, investing, budgeting, or long-term financial planning.

Research Context

This article draws on research from behavioral economics, psychology, neuroeconomics, consumer behavior, and household financial well-being to explain why emotional spending can feel rewarding in the moment and why regret may appear afterward.

The analysis is informed by foundational work on decision-making under uncertainty, including Kahneman and Tversky’s research on prospect theory and loss aversion, which helps explain why later discomfort can feel stronger than the brief pleasure associated with a purchase. It also considers research on self-control, cognitive load, and emotional regulation, including work by Baumeister, Vohs, Tice, and Gross, to show how stress, fatigue, and emotional pressure can shift financial decisions toward immediate relief.

The article also uses insights from neuroeconomics and reward research, including studies by Knutson, Bossaerts, Rick, Wimmer, Prelec, and Loewenstein, to explain how anticipation, dopamine, reward systems, and symbolic meaning can make spending feel emotionally powerful before the long-term financial consequences are fully evaluated.

To understand regret, guilt, and shame, the article draws on cognitive dissonance theory, regret research, and moral psychology, including contributions from Festinger, Zeelenberg, Pieters, and related social psychology literature. These sources support the article’s central argument that financial regret is not simply evidence of personal failure, but a signal of conflict between short-term emotional relief and longer-term financial priorities.

The article also considers how modern consumption environments shape emotional spending. Research on choice architecture, digital friction, consumer behavior, and behavioral design helps explain why online shopping, personalized offers, urgency language, saved payment details, and fast checkout systems can reduce reflection time and intensify emotional decision-making.

Finally, the discussion is contextualized through institutional research on financial well-being, including reports from the Federal Reserve Board, which show that money decisions are shaped not only by income or objective resources, but also by stress, insecurity, perceived control, and subjective financial experience. Within the HerMoneyPath editorial framework, these sources support a non-punitive, evidence-based interpretation of emotional spending as a human financial pattern shaped by emotion, context, environment, and social expectations.

References

(APA — 7th edition)

Ariely, D. (2008). Predictably irrational: The hidden forces that shape our decisions. HarperCollins.

Baker, S. M., & Gentry, J. W. (2014). Consumer vulnerability. In T. L. Childers & C. Pechmann (Eds.), Handbook of marketing and society (pp. 1–24). Sage Publications.

Barrett, L. F. (2017). How emotions are made: The secret life of the brain. Houghton Mifflin Harcourt.

Baumeister, R. F., Vohs, K. D., & Tice, D. M. (2007). The strength model of self-control. Current Directions in Psychological Science, 16(6), 351–355. https://doi.org/10.1111/j.1467-8721.2007.00534.x

Deci, E. L., & Ryan, R. M. (2000). The “what” and “why” of goal pursuits: Human needs and the self-determination of behavior. Psychological Inquiry, 11(4), 227–268. https://doi.org/10.1207/S15327965PLI1104_01

Dittmar, H. (2005). A new look at “compulsive buying”: Self‐discrepancies and materialistic values as predictors of compulsive buying tendency. Journal of Social and Clinical Psychology, 24(6), 832–859. https://doi.org/10.1521/jscp.2005.24.6.832

Festinger, L. (1957). A theory of cognitive dissonance. Stanford University Press.

Folbre, N. (2001). The invisible heart: Economics and family values. The New Press.

Gennaioli, N., Shleifer, A., & Vishny, R. (2018). A crisis of beliefs: Investor psychology and financial fragility. Princeton University Press.

Gross, J. J. (2015). Emotion regulation: Current status and future prospects. Psychological Inquiry, 26(1), 1–26. https://doi.org/10.1080/1047840X.2014.940781

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291. https://doi.org/10.2307/1914185

Knutson, B., & Bossaerts, P. (2007). Neural antecedents of financial decisions. Journal of Neuroscience, 27(31), 8174–8177. https://doi.org/10.1523/JNEUROSCI.1564-07.2007